segunda-feira, 29 de fevereiro de 2016

Donald Trump, Viktor Orban and the west’s great walls

Tear down this wall” demanded Ronald Reagan in Berlin in 1987. “Build the wall” demands Donald Trump, the man poised to take over Reagan’s party by winning the Republican nomination for the US presidency in 2016.

While America is still debating Mr Trump’s demand for a “great, great wall” along its border with Mexico, Europe has already entered the wall construction business. The EU’s panic over the “migrant crisis” is leading to a multiplication of new physical barriers and checks in Europe, to block the passage of would-be refugees.

Once again, there are some painful historical ironies. The first breaches in the Iron Curtain in the summer of 1989 came when the Hungarian government removed the electric fencing that separated its country from Austria — a decision that set off a train of events that culminated in the fall of the Berlin Wall a few months later. A quarter of a century on, Hungary has once again been a trailblazer, but this time in the opposite direction. When Viktor Orban, Hungary’s prime minister, built a razor-wire fence along his country’s frontier last summer, to deter would-be refugees, he was roundly denounced. A few months later, an Orban-style fence has just been built along the Greek-Macedonian border, and frontier controls are being tightened across Europe.

The journey from Reagan to Trump — from tearing down walls to putting them up — says a lot about the west’s journey from confidence to fear over the past 30 years. There are many reasons for this new demand for barriers between the west and the rest. The most obvious and direct cause is the fear of mass immigration from what used to be called the “third world”. But, beyond that, there is a broader loss of faith in the west’s ability to engage successfully with the outside world.

Even before the migrant crisis, anti-immigration parties were on the rise across Europe. They are almost certain to gain strength amid the present panic. Europe’s extreme right is already hailing the rise of Mr Trump, on the other side of the Atlantic. Jean-Marie Le Pen, the founding father of France’s National Front, recently tweeted: “If I were American, I would vote for Donald Trump — may God protect him.” Concerns about immigration from the Muslim world and terrorism have been linked in both Europe and the US — and taken to the extreme by the Trump campaign’s ugly demand for a temporary ban on all Muslims entering the US.

Beyond the fears about mass migration, however, there is also a crumbling of some of the ideas that have underpinned western engagement with the outside world since the end of the cold war. The first principle is the promotion of a “globalised” economy through the removal of barriers to trade and investment. The second is a willingness to contemplate foreign military intervention in the world’s trouble spots.

These two ideas — globalisation and liberal interventionism — were indirectly linked. The best solution to poverty and instability in the non-western world was (and is) routinely said to be economic growth, through increased trade and investment. But, in the aftermath of the fall of the Berlin Wall, western powers also became more willing to contemplate military intervention to “stabilise” failed states and troubled regions that had proved impervious to the magic of globalisation — from the Balkans to Africa and Afghanistan.

After 25 years of governments running these policy experiments, however, western voters seem increasingly sceptical about both globalisation and liberal interventionism. In the aftermath of the Iraq and Afghan wars, there is very little appetite for further large-scale western military intervention in the Middle East. All the Republican candidates in the presidential race are prepared to pile into President Barack Obama for “weakness” in Syria, but none are proposing the deployment of ground troops. Similarly, while there is anguish inside the EU about the influx of refugees from Syria, there is no discussion of sending troops there to end the conflict that is driving the refugee flows.

New trade agreements are also going out of fashion. Four years after the fall of the Berlin Wall, President Bill Clinton signed the North American Free Trade Agreement with Mexico and Canada. Now Mr Trump is proposing not just to build a wall along the Mexican frontier, but to impose swingeing new tariffs on US manufacturers based in Mexico. Even Hillary Clinton, the Democratic frontrunner, is making protectionist noises on the campaign trail. And while political leaders in the EU claim to be in favour of negotiating a new trade deal with the US, the European left is already mobilising the public against the idea. Even Europe’s cherished internal market may now be threatened by the reimposition of frontier controls within the EU’s border-free Schengen zone.

Viewed from the comfort of Europe or the US, the problems of the Greater Middle East, Africa or Central America increasingly look both frightening and insoluble. If neither trade nor military intervention can succeed in creating prosperity and order, then the temptation increases to create physical barriers to keep the rest of the world at bay.

Mainstream politicians in both the EU and the US will continue to argue that building barriers is not the solution to the problems of the world or the west. But they are in danger of finding that their voters have stopped listening.

Gideon Rachman

Fonte: FT

sexta-feira, 26 de fevereiro de 2016

Britons’ maths-phobia is no laughing matter

As Britain struggles to work out whether it is better off in or out of the EU, it might pay heed to the devastating analysis that shows the really frightening obstacles to a thriving future lie at home. The OECD, the Paris-based think-tank, last month ranked British teenagers bottom of 23 developed countries in literacy, and 22nd out of 23 in numeracy.

That was not the first blow. Another OECD survey in May put British 15-year-olds 20th in the world in maths and science (above the US at 28th, it must be said); Singapore was top, followed by Hong Kong and South Korea. International rankings are controversial, not least because they sometimes compare cities or regions against whole countries; Shanghai’s glittering record hardly reflects the performance of China’s rural poor. Still, the tables help monitor a country’s progress, or lack of it — and point to teaching techniques that can be borrowed.

The consequences of failing in maths are crippling. Skills in the subject, from the most basic to the sophisticated, matter for every country. You might start with productivity, wages and growth, in a world where “every job will be digital”, a vision that applies to nursing, construction or farming as much as to web design. It also matters for social mobility and exclusion, and for the ability of citizens to cope with life, from reading an aspirin bottle, to the challenges of budgets, credit, savings and pensions.

In Britain, the numeracy problem seems peculiarly entrenched. Over the past couple of decades performance has stalled or drifted down. Successive governments, task forces, campaigns and initiatives by schools have all identified maths skills as essential and hurled themselves at the task of improvement. There are indeed signs of success, yet nothing on the scale needed.

The problem begins with a culture in which it is acceptable to remark “I don’t do numbers”, as if it’s a matter of DNA. It might be thought endearing of Prince Harry to say: “I hope I’ve got the physical skills to fly a helicopter. But mentally, there are the exams and everything — I mean, I can’t do maths.” It should be less so that Gordon Brown, who ran the UK economy for a decade as chancellor, once joked to school pupils: “I did maths for one year at university but I don’t think I was ever very good at it, and some people would say it shows.”

But the quote that best captures the British disease is from Benedict Cumberbatch, the actor, who with a nod to his role in The Imitation Game offered consolation to those struggling with maths as he did at Harrow, an exclusive school: “You can pretend to be Alan Turing.” Not if you need a job that offers a reliable wage and a career, you can’t.

It’s true that a small proportion of people struggle profoundly to grasp what numbers are at all. Some years ago, prompted by discussions of whether anyone could master basic maths if taught well, I set out to talk to those who work with “dyscalculia”. Watching a seven-year-old girl struggle to see that seven plus one is eight can give you a sense of vertigo, challenging you to explain what you take for granted.

Researchers have noticed a difference in five-month-old babies; if an adult plays peekaboo, bringing out one toy again and again, most babies will laugh or look alert if suddenly two toys appear — but a very few will not react at all. Yet even if there is a dispute about the exact percentage affected, most agree it is low.

For everyone else, basic mastery up to a good level at age 16 should be possible. But in Britain for several decades, an assortment of obstacles has emerged. Lack of specialist primary schoolteachers is a big concern; many are generalists and not confident with maths, in contrast, say, with Chinese counterparts, who are specialists and teach in teams, returning repeatedly to children who have not mastered a technique until they have.

Waves of enthusiasms have produced a patchwork of different techniques. There is a long-running tussle between those who advocate mastery of basic skills and those who want to focus on “understanding”. The long ideological battle about the value of testing has added its own confusions.

The OECD has praised reforms such as raising standards of qualifications at 16, and devising new ones to enable teenagers to study maths for longer. Currently only one in eight of British teenagers do maths after 16, putting the country far behind other developed nations.

But Britain arguably needs between 10,000 and 20,000 more maths teachers — and many more maths lessons each week, drawing on Asian comparisons. Teachers in many countries grappling with this argue that we are long overdue a review of the skills that pupils really need to master in the 21st century. Less trigonometry and factorising quadratic equations, say, and more percentages, fractions, probability and statistics — and matrices, which are rich in digital applications.

Above all, we need a change of culture. Last year, after protests, L’Oréal Paris withdrew an advert for an anti-ageing cream in which the actor Helen Mirren gave the pay-off line: “Age is just a number. And maths was never my thing.” If those ads are not going to be made in the first place, the campaign has some way to go.

Bronwen Maddox is editor of Prospect

Fonte: FT

quarta-feira, 24 de fevereiro de 2016

The Chinese chronicle of a crash foretold

The highway leading to the birthplace of Mao Zedong in central China is lined with forests of half-built or empty apartment towers. On your way to pay homage to the Great Helmsman you can visit the spot where, less than three years ago, an ambitious local billionaire flew in on his private helicopter amid great fanfare and broke ground on what was meant to be the world’s tallest building: the 838m Sky City. Today the excavated foundations lie submerged in a makeshift fish farming pond.

Economists have long pondered the so-called skyscraper curse, the uncanny correlation between construction of the world’s tallest building and an accompanying financial crash. From the end of Roaring Twenties America to the bursting of the credit boom in the sands of the Gulf, the Empire State Building (started in 1930), Sears Tower (started in 1970), Petronas Towers (completed in 1996) and the Burj Khalifa (completed in 2009) have foretold or coincided with crises — apparent signs that irrational exuberance can manifest itself in physical form.

Today, some analysts describe the Chinese real estate market as the single most important sector in the global economy — and the biggest risk factor. This is less fantastic than it sounds when you consider that in two years — 2011 and 2012 — China produced more cement than the US did in the entire 20th century.

Because of this, the fate of everything from Hong Kong financial institutions to German carmakers to Australian miners is now in the hands of homebuyers in places like Changsha, the city where Sky City was supposed to be built.

In recent years, overbuilding has been encouraged by local officials, who collect large portions of their revenue from land sales. The results can be seen across China: from ghost cities looming out of the frozen Manchurian plains to the fringes of Lhasa, where Tibetan nomads graze yaks in the yards of empty luxury villas.

China’s economy is extraordinarily reliant on investment, which accounts for nearly half of the country’s gross domestic product. But slowing investment in Chinese real estate in the past two years has contributed to a collapse in global prices of commodities and declining growth in raw material exporters such as Australia, Brazil, South Africa and Indonesia.

The building boom of recent years has led to enormous excess inventory but the true scale is impossible to estimate because developers and local governments are offered incentives to under-report the problem. Despite a slowdown in 2015, real estate investment in China rose by 1 per cent, even as average house prices in the 70 largest cities fell.

Similarly, Chinese commodity imports in volume terms increased last year, as price collapses caused a large import contraction in value terms.

In other words, China’s economy has slowed by a couple of percentage points and global commodity prices have plummeted even before any correction in the country’s property sector begins in earnest. An outright decline in real estate investment, which is surely coming, will also have profound implications for the rickety, debt-laden Chinese financial system. Analysts estimate that more than 60 per cent of Chinese bank loans are directly or indirectly tied to real estate.

With a debt-to-GDP ratio that is higher than the US and Germany, serious trouble in the Chinese property sector would send shockwaves round the globe and make the recent fallout from declining Chinese currency and equity markets look like a minor squall.

Local governments in places like Changsha have started to recognise that many of the shoddily built, overpriced apartments will never be sold. But their response is alarming from the perspective of the wider economy .

According to officials in several Chinese cities, their solution is to break ground on entirely new districts and to offer land to “better quality” property developers at marked down prices. The hope is that developers will abandon the existing empty blocks, and build higher quality apartments that can be sold to consumers for big discounts because of the lower land costs.

In the twisted incentive structure of Chinese officialdom, this is rational because it will prompt the flow of fresh finance, revive land revenues and boost GDP. But if that sort of thinking prevails, it may turn out that merely breaking ground on Sky City was enough for the skyscraper curse to fall on China.

Jamil Anderlini

Fonte: FT

quinta-feira, 18 de fevereiro de 2016

French spelling wars are a displacement activity

In a nation still reeling from its worst-ever terrorist attack, where the far right regularly garners 30 per cent of the vote and where youth unemployment hovers around 25 per cent, it might seem puzzling that the big political debate this month in France should centre on the possible abolition of the circumflex accent.

Yet I was not surprised that an old spelling reform, first put forward in 1990 by the Superior Council of the French Language and approved by the formidable and neophobic Académie Française, should have stirred up more moral outrage on Twitter than any government measure since the beginning of the year. As Napoleon wrote from exile on the island of St Helena: “France is French when it is well written.” The French language is the seat of the French soul and you mess with it at your peril.

So there is no new reform. There is simply a government “announcement” about the imminent application of the original reform in schools from September. We are in the realm of spin, and that spin involves Najat Vallaud-Belkacem, who is being pushed into the limelight in her dual capacity as education minister and cherished symbol of French cultural assimilation. But why all this passion unleashed for the circumflex in maîtresse, for the rogue — and mute — “i” in oignon, for the baffling second acute accent in événemen t?

The passion and outrage appears to be most voluble among the educated over-40s. (Anyone younger or less educated seems to have other poissons à frire than rallying round the hashtag, je suis circonflexe.) The reason for this, I think, is that ever since François I first standardised the language, correct usage has been an indication of quality, both social and moral.

For example, politicians who speak bad French tend to be mistrusted. For an entire week in the run-up to the 2007 presidential elections, the media was fascinated by Ségolène Royal’s use of the word bravitude to mean “bravery” (it was a neologism of her own invention), as opposed to the evocative and chivalric word, bravoure. Her opponents seized on this as proof of her unsuitability for the highest office. A president, it was pointed out, had to speak French that was “pure and irreproachable”.

This logocentric snobbery is not a left-right thing. President François Hollande and his cronies, at their summer dinner parties in the Lubéron, will delight just as much as their rightwing counterparts on the Côte d’Azur, in a little punning and subjunctive sparring. This generation retains in its DNA the horror — inherited from the merciless court system of the ancien régime — of appearing stupid. As such it prefers wit to humour, which is not the case for most younger French people.

In this naturally conformist culture, where everyone tends to dress the same, correct spelling is much more of a social marker than clothes are. If you make spelling too easy, you take away a deliciously discreet proof of distinction. In France, a society built on the idea of equality which is at the same time deeply hierarchical, these subtle markers of refinement can exist without revealing the huge gaps that exist between that egalitarian ideal and the reality. For despite its formidable, educated elite with its dizzying grasp of the imperfect subjunctive, international studies show that French school children are floundering.

Why is this happening now? Its language is one of France’s most powerful totems, and French spelling, which is predominantly etymological rather than phonetic, locks history inside it in a way that English does not. It is unfortunate, however, that minds should be distracted by this skirmish while the government prepares to modify the constitution in order to remove the citizenship of French-born bi-nationals found guilty of “a crime that represents a serious threat to the life of the nation”.

Lucy Wadham is author of ‘The Secret Life of France

Fonte: FT

quarta-feira, 17 de fevereiro de 2016

Fed must act on ‘economic anger’, says official

The US Federal Reserve must do a better job of responding to the rising tide of economic anger in America that is leading to a surge in protectionist rhetoric on the presidential campaign trail, according to the newest member of its policy committee.

In an interview with the Financial Times, Neel Kashkari, who took over as head of the Minneapolis Federal Reserve at the start of the year, warned that the Fed needed to work harder to rebuild public trust and communicate with American citizens. Economic anger, he said, was “all around the country and it is non-partisan”.

Mr Kashkari’s first public forays this week have quickly positioned him as an outspoken voice among the central bank’s policymakers.

As a senior treasury official in the administration of George W Bush and the first Obama administration, Mr Kashkari was a key architect of Wall Street’s 2008 bailout. But on Tuesday, in his first speech since joining the Minneapolis Fed, he called for regulators to consider breaking up the largest US lenders, which he said remained “too big to fail”.

In his interview with the FT he blamed the bailouts he oversaw as one of the “root causes for the loss of trust” in the US’s economic managers. Those actions had “really violated a core American belief” that risk takers had to bear the consequences of things going wrong, he said, and “it really leads to great anger if you violate the core beliefs of a society”.

The impact, he said, had been made worse by a history of opacity at the Fed and a past institutional reluctance to explain monetary policy clearly to the American public.

The Fed was now paying the price for decades of “very poor” communications during which it “adopted this Wizard of Oz routine that ‘We are so mysterious and you can’t understand what we are doing’,” he said, “and that really hurt trust between the people and the institution”.

Anger about the economy was also fuelling support for those advocating the erection of new barriers to protect US industry. “I don’t think protectionism is the right path. I think we need to promote free markets around the world. But some of the anger is understandable,” he said.

“We need to promote free markets on both sides. It can’t just be the American economy that is free and our trading partners are not free. So I understand that anger that is there. We need to push back against that [protectionist rhetoric] but also push out globally for free markets everywhere.”

His words come amid a presidential election campaign that is being dominated by frustration among voters about the sluggish growth since the 2007-09 financial crash. Some 72 per cent of the electorate feels the economy is still in recession, according to the American Values Survey released in November — even though economic analysts date the Great Recession as having ended in mid-2009.

That frustration has spilled over into antipathy towards the Fed itself, which is being expressed on both sides of the political divide. Democratic lawmakers have questioned the central bank’s decision to lift interest rates, warning it could stifle wage growth, while Republicans are calling for greater scrutiny of the Fed’s decisions amid lingering anger over the scale of its interventions during the crisis.

But above all it has helped fuel the rise of populist candidates such as Bernie Sanders, a self-described democratic socialist, and Republican frontrunner Donald Trump, both of whom have called for the US to do more to protect its own industry from cheap imports and foreign competition, and found support for those policies.

Mr Kashkari praised the work of Janet Yellen, the current Fed chair, in speaking directly and candidly in explaining the central bank’s policies, but said the central bank needed to go even further still.

Mrs Yellen was “trying to do the right thing for the country”, and if people got to know her and other people across the Fed system “they would be very proud we have this institution in our country”. However, he added, “we don’t really let them see in”.

“I think we could do a better job,” he said. “The press conferences [held quarterly by the Fed chair] are a step in the right direction and Chair Yellen is very candid in those press conferences and addresses the questions directly. That’s positive.”

But the Fed needed to “look for more opportunities like that. It has to happen on all levels.”

Monetary policy was hugely complicated, and it was not possible to explain every twist and turn of the debate to the whole population. That meant it was critical that the public trusts the central bank, he explained.

“You are not going to have the population as a whole understand all the nuances of what we are talking about here. They need to trust us. They need to know that we care. If they trust us and know that we care, they are going to give us the benefit of the doubt on some of the complexities they may not fully understand.”

Fonte: FT

sexta-feira, 12 de fevereiro de 2016

Negative US interest rates take banks through the looking glass

Afew days ago, I attended a financial conference with a large collection of some of the most powerful and savvy asset managers in America. When asked to vote about the likely path of US interest rates, almost two-thirds of the participants suggested that the Federal Reserve would cut rates this year, rather than keep them neutral (or raise them).

Yes, you read that right. Less than two months ago, the Fed finally embarked on its long-awaited (and heralded) tightening move. It then signalled that it expected to see four rate rises this year. While investors did not entirely accept this, the Fed Funds futures market suggested that two, not four, rises were likely in 2016.

But if the group of investors I saw was representative (and I think they are), a US rate cut is now the majority view. Talk about a mood swing; this makes a teenager look consistent.

Is this justified? In economic terms, I would argue not. After all, the fundamental US economic data have not moved so wildly in recent weeks. On the contrary, as Janet Yellen, the Fed chair, pointed out in testimony to Congress on Wednesday, growth is still fairly steady and the wider global picture is far from disastrous. Unsurprisingly, she emphasised that she still thinks that rates are on a modest upward trend.

But what is also clear is that this swing in views does not just reflect macroeconomic signals. On the contrary, subtle shifts in global capital flows are creating volatility. Moreover, market sentiment is now displaying what billionaire investor and philanthropist George Soros has described as “reflexivity” — prices fall, so people get frightened, and then prices fall further.

Behind all this is a debate about whether the US could soon follow Japan and Switzerland and produce negative interest rates.

That used to be the stuff of late night bar-room chats between economists. But the fact that Japan has moved into negative territory (after Switzerland) has changed all that. Another development has also had an enormous symbolic effect: the Fed has just launched its annual stress test of the banks, and asked the largest ones to model for the first time how their balance sheets could look with negative rates. (Specifically, they have been asked to model an “adverse market scenario” where three-month treasury bills tumbled to minus 0.5 per cent for a long period.)

The Fed has stressed that this is “hypothetical”. And it is not an entirely unprecedented idea: short-term rates have tumbled briefly below zero in the US before. No matter. The symbolism of this in the Wall Street echo chamber is extraordinarily powerful: what was once almost unimaginable is actually being imagined — and tangibly measured. And this is frightening for investors for at least two reasons.

First, and most obviously, a world with rates below zero is one in which normal economic relationships are apt to break down. In such a world, it feels as if all manner of taboos might tumble, so it is hard to set mental boundaries.

Until recently, it was widely assumed among investors that even if central banks did cut rates, these could not fall below minus one per cent. But this week JPMorgan issued a piece of research which suggests that central banks now have the technical tools to cut rates to minus 4.5 per cent in the eurozone, minus 3.45 per cent in Japan, minus 2.7 per cent in the UK and minus 1.3 per cent in the US. But nobody knows any more if even that (unlikely) scenario is the floor.

Secondly, as investors confront this bewildering Alice in Wonderland world, they are also discovering great “known unknowns” in the system: nobody knows what this means for banks. Or as the Bank of America Merrill Lynch observed: “Modelling the negative rate scenario is extraordinarily difficult . . . [since] predicting how Libor would behave in a negative environment is a difficult question.”

The good news is that investors may eventually adapt; the idea of negative rates in Switzerland, for example, no longer shocks. The bad news, however, is that this could take a long time. And the path of the underlying economic data looks dangerously patchy.

Either way, two things are now clear: first, this volatility is unlikely to vanish any time soon in a world of increasing reflexivity; and second, the Fed will need to play an astonishingly canny hand in the coming weeks.

One place to start would be for it to commit to publishing the results of those novel stress tests on negative rates as quickly as possible — and with all the details. The Fed cannot afford to let market imaginations run (any more) wild.

Gillian Tett

Fonte: FT

quinta-feira, 11 de fevereiro de 2016

The petrodollar age is no more but with it go old certainties

Vladimir Putin, the Russian president, is being forced to consider a fire sale of state assets even as he steps up the bombing of opposition forces in Syria. Waging a war of words with Iran, Saudi Arabia is planning its debut on international bond markets. Nigeria has started talks about assistance from the World Bank. Venezuela careers from bust to bankruptcy. Welcome to the world of $30 oil.

Conversations about the oil market once started from two ironclad assumptions. Cheap oil was good for global growth because consumers are more inclined than producers to spend windfall gains and disturbances in the Middle East would send prices higher so the west should back the Arab autocrats who kept the wells pumping.

Received wisdom has been upended. The fall from $100 a barrel in 2014 should have seen consuming nations throwing their hats in the air. Not a bit of it. Europe, beset by stagnation and overwhelmed by refugees, has other things on its mind. The US, now producer as much as consumer, is stuck with anaemic growth. China, the world’s thirstiest economy, has its own challenges. Global equity markets have tumbled in tandem with the oil price.

The geopolitics are likewise counterintuitive. Prices have fallen even as fighting in Iraq, Syria, Yemen and Libya has escalated. Saudi Arabia, once the guarantor of a floor price, now deploys higher output as a weapon against Iran. The nuclear deal with Iran has left the west torn between the old allegiance to Riyadh and the allure of detente with Tehran.

The third law of oil — that price falls are always cyclical diversions from an inexorable rise — looks shaky. The accumulating evidence points to a structural shift that will keep prices relatively low. During the century before the great price shock of the early 1970s the real cost of a barrel of oil was between $10 to $40. Economists at Llewellyn Consulting in London make a convincing case that this trading range offers a rough template for the future.

The 1970s shock rewrote the rules of international relations. The Middle East became a focus of geopolitical attention. The Soviet Union was given a new, albeit shortlived, lease of life. Venezuela, Brazil, Mexico and Nigeria were among those blessed — or perhaps cursed — by soaring prices. Now reimagine this landscape in an era of permanently cheap oil. Some producers doubtless will fare better than others but the power of the petrodollar has gone.

My sense is that western foreign policymakers are still clinging to the idea that nothing much has changed. Low prices will be disruptive — dangerously so in places — but temporary and thus unlikely to alter the geopolitical balance much. Producers will get their act together, high-cost wells will go out of business and the return of global growth will see the price rise again. The doctrine of “peak oil” — that a finite supply of hydrocarbons over time will always pull prices upwards — has its devotees.

Doubtless there will be price spikes but there are strong reasons to suppose the rules have changed. A decade ago, the US was the world’s largest oil importer. Shale oil and gas now assure it of energy self-sufficiency during the 2020s. Shale wells can be capped and uncapped relatively cheaply, providing a shock absorber in international markets. Saudi Arabia remains a swing producer but the “swing” has lost its force.

Opec has been enfeebled. A 1 per cent cut in oil output should push up prices by 10 per cent in the short term, but no single supplier has enough capacity to increase revenues by cutting output. The result is a free-for-all fight for market share. As Llewellyn Consulting puts it, Opec now more closely resembles a secretariat than a cartel.

Environmental laws and alternative energy sources conspire against hydrocarbons. You do not have to believe that governments will meet their climate change targets to forecast an accelerating shift into renewables and alternative energy sources, whether electric cars or solar power. Energy efficiency is pressing in the same direction.

All this means that policymakers should be thinking a lot harder about the geopolitics.

There is not much that is reassuring for a world already described by its insecurities. Whatever the theoretical benefits, the scale and speed of the oil price drop has added another destabilising twist to the forces driving fragmentation and conflict.

Russia, facing powerful economic and demographic headwinds, will be weakened further. Events in Syria suggest Mr Putin may be more threatening for that.

Declining powers can be more dangerous than rising ones. Falling state revenues threaten to undercut the strides made by Nigeria in fighting corruption and the security threat from Boko Haram. The last oil price collapse was among the triggers for civil war in Algeria.

Cheap oil sharpens the Sunni-Shia confrontation in the Gulf, could undermine fatally the Iraqi government and is weakening the Kurds fighting Isis. It may also hasten US and European disengagement from the region. Why get involved if they do not need the oil?

Like the cold war, the petrodollar age imposed a predictability on the world. It would be absurd to lament its passing but just as unwise to ignore the consequences. We may discover soon enough that $30 oil comes with another type of price.

Philip Stephens

Fonte: Philip Stephens

sexta-feira, 5 de fevereiro de 2016

Why it would be wise to prepare for the next recession

What might central banks do if the next recession hit while interest rates were still far below pre-2008 levels? As a paper from the London-based Resolution Foundation argues, this is highly likely. Central banks need to be prepared for this eventuality. The most important part of such preparation is to convince the public that they know what to do.

Today, eight-and-a-half years after the first signs of the financial crisis, the highest short-term intervention rate applied by the Federal Reserve, the European Central Bank, the Bank of Japan or the Bank of England is the latter’s half a per cent, which has been in effect since March 2009 and with no rise in sight. The ECB and the BoJ are even using negative rates, the latter after more than 20 years of short-term rates of 0.5 per cent, or less. The plight of the UK might not be that dire. Nevertheless, the latest market expectations imply a base rate of roughly 1.6 per cent in 2021 and around 2.5 per cent in 2025 — less than half as high as in 2007.

What are the chances of a significant recession in the UK before 2025? Very high indeed. The same surely applies to the US, eurozone and Japan. Indeed, the imbalances within the Chinese economy, plus difficulties in many emerging economies, make this a risk now. The high-income economies are likely to hit a recession with much less room for conventional monetary loosening than before previous recessions.

What would then be the options?

One would be to do nothing. Many would call for the cleansing depression they believe the world needs. Personally, I find this idea crazy, given the damage it would do to the social fabric.

A second possibility would be to change targets, possibly to ones for growth or level of nominal gross domestic product or to a higher inflation rate. It would probably have been wise to have had a higher inflation target. But changing it when central banks are unable to deliver today’s lower target might destabilise expectations without improving outcomes. Moreover, without effective instruments a more ambitious target might just seem empty bombast. So the third possibility is either to change instruments or to use the existing ones more powerfully.

One instrument, not much discussed, would be to organise the deleveraging of economies. This might need forced conversion of debt into equity. But, while desirable in extreme circumstances, this would be practically difficult.

Another would be a still bigger scale of quantitative easing. At the end of the third quarter of last year, the BoJ’s balance sheet was 70 per cent of GDP, against less than 30 per cent for the Fed, the ECB and the BoE. The latter three could follow the former. Moreover, the assets they buy could be broadened, one possibility being foreign-currency bonds. But that would be provocative and unnecessary. The BoJ and ECB have engineered big currency depreciation without making it quite so blatant.

Yet another instrument is negative interest rates, now used by the ECB, the BoJ and the central banks of Denmark, Sweden and Switzerland. With clever gimmicks, it is possible to impose negative rates on bank reserves at the margin, thereby generating negative interest rates in markets, without imposing negative rates on depositors. How far this can be pushed while cash is still an alternative is unclear. Beyond a certain point, people seek to move into cash-backed warehouse receipts, unless a penal tax were imposed on withdrawal from banks or cash were abolished altogether. Moreover, it is unclear how economically effective negative rates would be, apart from lowering the currency.

A final instrument is “helicopter money” — permanent monetary emission for the purpose of promoting purchases of goods and services either by the government or by households. From a monetary point of view, this is the equivalent of intentionally permanent QE. Of course, actual QE might become permanent after the event: that is now likely in Japan. Again, supposedly permanent monetary emission might turn out to have been temporary, after the event. But if the money went directly into additional spending by government or into lower taxes or to people’s bank accounts, it would surely have an effect. The crucial point is to leave control over the quantity to be emitted to central banks as part of their monetary remit.

Personally, I would prefer the last instrument. But at this stage it is crucial to recognise the great likelihood that something even more unconventional might have to be done next time. So prepare the ground beforehand. Central banks should be filling in these blanks now, not after the next recession hits.

Martin Wolf

Fonte: FT

quarta-feira, 3 de fevereiro de 2016

The messy aftermath of the Fed’s mistake on the interest rate

December 16 2015 may go down as the date of one of the most monumental policy errors in history. The financial markets were nervously anticipating that the US Federal Reserve would raise the interest rate for the first time in nearly a decade — but few grasped the inadequacy of the data driving the decision.

The Fed had never before initiated a tightening cycle when the manufacturing sector was shrinking. Moreover, US corporate borrowers had begun reducing their debts, according to Morgan Stanley; in previous cycles, the Fed had tightened to cool credit cycles.

Of course, the Fed is not obliged to pursue any economic objectives beyond its two formal mandates of stable prices and maximum employment. In late 2012, when a third round of quantitative easing was launched, the unemployment rate was 7.8 per cent. It must have seemed a safe bet to undertake a commitment to stop easing when it fell to 6.5 per cent. Safe, that is, until the target was achieved sooner than the markets were willing to give up their stimulus.

It was no coincidence that in the first half of 2014 the Fed unveiled a tracking index to better capture the health of the jobs market. The labour market conditions index is derived from indicators including obscure metrics such as the micro-gauge favoured by Janet Yellen, Fed chair: the percentage of workers who voluntarily quit in a given month.

That August, with unemployment at just over 6 per cent, Ms Yellen addressed the central bankers’ symposium at Jackson Hole, Wyoming. She explained that, though the labour market had improved in the past year, the index suggested “the decline in the unemployment rate over this period somewhat overstates the improvement in overall labour market conditions”. In other words, give the stimulus more time.

With hindsight, few dispute that the Fed missed an opportunity to raise rates in 2014. No doubt, tightening policy at that stage would have created its own messy side-effects. That said, the benefits would have been significant.

First, for example, commodity prices might not have risen so high or so fast without the cheap money flowing from the US to emerging markets. Property prices worldwide might not be as frothy had investors not sought refuge in the sector from what they rightly recognised as risky valuations in equity and bond markets. And “fragile” would not now be the word for financial markets and economies worldwide. This fragility was laid bare in August after a minuscule currency devaluation by Beijing exposed systemic risk simmering just beneath the surface of intricately interconnected global markets.

History has shown time and again that labour market data are the most lagging and least predictive indicators. In the current instance, the data from the December jobs report are also misleading, given the lack of income being generated to propel consumption. A scant 3 per cent of jobs created in December went to those ages 25 to 55, with the balance going to cohorts that tend to work part-time for less pay.

For a more forward-looking indicator, Jonathan Basile of AIG tracks the University of Michigan’s survey of households’ unemployment expectations. The latest data show 29 per cent expect a higher rate in a year’s time — the worst outlook since September 2014.

The bond market, meanwhile, sees no shades of grey in the data; it is shifting rapidly from pricing in one rate hike this year towards pricing in the possibility of the next move being a rate cut, all but ridiculing the Fed’s insistence that four rate hikes would come to pass in 2016.

Tellingly, Fed officials are softening their tone on the number of times the rate might rise this year. “Don’t fight the Fed” — the idea that markets ultimately benefit from the Fed’s decisions — has become a cliché. The truth is the Fed has never dared fight the markets.

Danielle DiMartino Booth is president of Money Strong, an economic consultancy, and a former adviser to the Dallas Fed

Fonte: FT

terça-feira, 2 de fevereiro de 2016

Bring our elites closer to the people

In the opening contests of the 2016 race for the White House, Ted Cruz, a Republican candidate described as a “mountebank”, has upstaged Donald Trump, a “narcissist”. Meanwhile, Bernie Sanders, a self-proclaimed Democratic socialist, more or less tied with establishment favourite Hillary Clinton. So therebellion against the elites is in full swing. The vital question is whether (and how) western elites can be brought closer to the people.

We are not Chinese. Maybe even the Chinese will not remain content to hand responsibility for public affairs to a self-selecting elite. In the west, however, the idea of citizenship — that the public realm is the property of all — is not only of ancient standing; it has also been the object of an ultimately successful struggle in recent centuries. An essential attribute of the good life is that people enjoy not just a range of personal freedoms, but a voice in public affairs.

The outcome of individual economic freedom can be great inequality, which hollows out realistic notions of democracy. The governance of complex modern societies requires technical knowledge — and we already face the danger that the gulf between economic and technocratic elites on the one hand, and the mass of the people on the other, becomes too vast to be bridged. At the limit, trust might break down altogether. Thereupon, the electorate will turn to outsiders to clean up the system. We are seeing such a shift towards trust in outsiders not only in the US but also in many European countries.

A complacent view is that the disaffected may let off steam but the centre will hold. This is quite possible. But it is a risky strategy. If the disaffection grew worse, the centre might not hold. Even if it did, a democratic society in which a large minority is disaffected while a majority is full of distrust would not be a happy one. Yet such a gap has emerged between the attitudes of informed elites towards established institutions and those of the wider public.

So what are the root causes of this divide in attitudes? One is cultural change. Another is distaste over changes in the ethnic composition of nations. Then there is anxiety over rising inequality and economic insecurity. Perhaps the most fundamental cause is a growing sense that elites are corrupt, complacent and incompetent. Demagogues play on such sources of anxiety and anger. That is what they do.

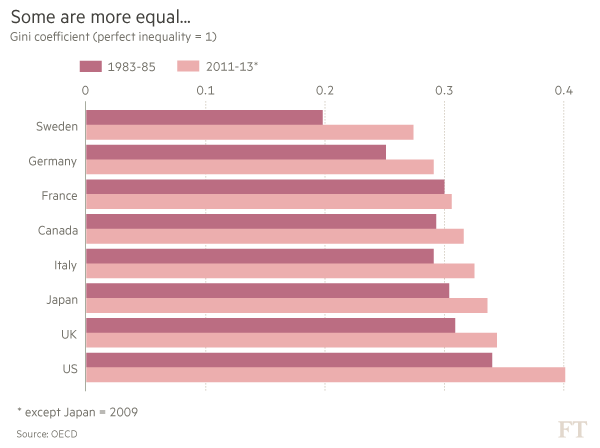

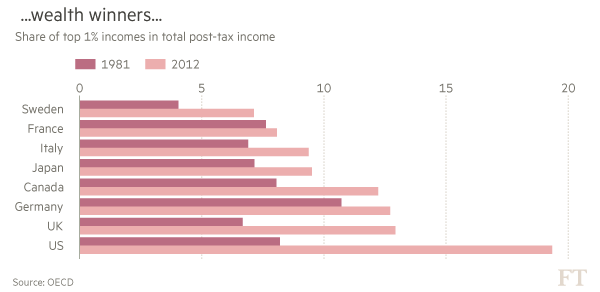

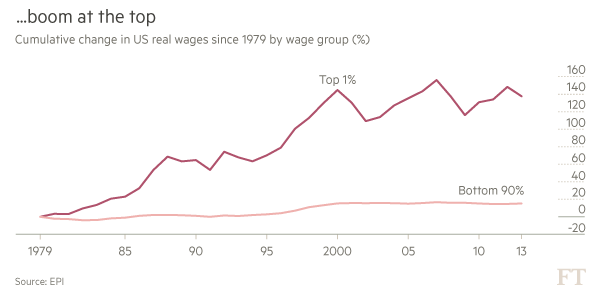

As a recent OECD note points out, inequality has risen substantially in most of its members in recent decades. The top 1 per cent have enjoyed particularly large increases in shares of total pre-tax income. This divergence between the success of the economic elite and the relative lack of success of the rest has been particularly striking in the US. Thus, notes the OECD: “Between 1975 and 2012 around 47 per cent of total growth in [US] pre-tax incomes went to the top 1 per cent.” As the US has developed a Latin American-style income distribution, its politics have grown infested with Latin American-style populists, of both the left and the right.

How should those in the centre respond? Successful politicians understand that the people need to feel their concerns will be taken into account, that they and their children enjoy the prospect of a better life and that they will continue to have a measure of economic security. Above all, they need once again to trust the competence and decency of economic and political elites.

Here are a few elements of what needs to be done. First, of all aspects of globalisation, mass immigration is the most disruptive. Movement across borders needs to be brought under control. The presence of 11m undocumented immigrants in the US should never have been permitted. In the case of Europe, regaining control of the borders is an overwhelming priority if the union is even to survive. Refugees must now be the priority. This demands creation of a significant European capacity to promote order beyond the bloc’s borders.

Second, the eurozone needs to embark on a fundamental questioning of its austerity-oriented macroeconomic doctrines. It is appalling that real aggregate demand is substantially lower than in early 2008.

Third, the financial sector needs to be curbed. It is ever clearer that the vast expansion of financial activity has not brought commensurate improvements in economic performance. But it has facilitated an immense transfer of wealth.

Next, capitalism must be kept competitive. We are in a new gilded age in which business exerts great political power. One response is to promote competition ruthlessly. This will require determined action.

Then, taxation must be made fairer. Owners of capital, the most successful managers of capital and some dominant companies enjoy remarkably lightly taxed gains. It is not good enough for business leaders to insist that they are sticking to the law. This is not an adequate definition of ethical behaviour. This view is particularly disingenuous when commercial interests play such a powerful role in shaping those laws.

In addition, the doctrine of shareholder primacy needs to be challenged. Shareholders enjoy the great privilege of limited liability. With their risks capped, their control rights should be practically curbed in favour of those more exposed to the risks in the company, such as long-serving employees. And, finally, the role of money in politics needs to be securely contained.

Western polities are subject to increasing stresses. Large numbers of the people feel disrespected and dispossessed. This can no longer be ignored.

Martin Wolf

Fonte: FT

Assinar:

Comentários (Atom)