sexta-feira, 31 de outubro de 2014

Bank of Japan opts for another dose of shock and awe

It was the day that “Abenomics” roared back.

On Friday morning, a report in the Nikkei newspaper that the national pension fund was poised to double its allocation to domestic stocks set pulses racing. But that was nothing compared with the excitement unleashed at 1:44pm, when the BoJ said it would crank up its already aggressive monetary easing programme, buying 60 per cent more bonds and tripling purchases of stocks to head off a recent slide in inflation.

The twin announcements did the trick, sending the yen to a new six-year low of 110.9 against the US dollar while pushing the Nikkei 225 stock average up almost 5 per cent, the biggest daily rise since last year’s “taper tantrum”.

For investors in Japanese assets, the one-two punch was a reminder that the key institutions are lined up squarely behind the prime minister in his mission to haul Japan out of more than a decade of deflation.

For the vast Government Pension Investment Fund, a shift to 50 per cent stocks – half domestic, half foreign – would surely be criticised as playing games with Y127tn ($1.15tn) of pensioners’ money.

But for the markets-minded administration of Prime Minister Shinzo Abe, there are few better ways of pumping up stocks, which have sagged in the wake of April’s increase in consumption taxes, while keeping downward pressure on the yen.

As for the BoJ, its supersized purchases of government bonds, up to Y80tn a year from Y50tn, will further bolster the bond market, just as the GPIF is paring its holdings.

And in the same week that the US Federal Reserve brought a formal end to its own asset-purchases, the effects on the yen will surely linger.

“Top-down leadership is back,” says Jesper Koll, head of equity research at JPMorgan. The BoJ’s move “hints at full integration of GPIF asset allocation reform with monetary policy,” he says, while underlining the bank’s role as a “committed JGB buyer of last resort”

The recent softening in the core consumer price index, dropping from 1.5 per cent in April to 1 per cent in September, had caused analysts to wonder if the BoJ should go more micro than macro.

One way of strengthening inflation expectations, for example, is to target communications towards people in their 20s and 30s, who tend to be more sceptical that prices can keep rising.

There was also a lot of talk about the BoJ stealthily rolling back its roughly two-year timeframe to allow itself more time to bring inflation up to its target of 2 per cent.

Instead, 18 months on from the birth of QQE, the BoJ has opted for another dose of shock and awe.

Mr Abe, facing a tricky decision in December on whether to raise taxes again, will want to ride the rally for as long as he dares.

Ben McLannahan

Fonte: FT

quinta-feira, 30 de outubro de 2014

...Melhor colocar as barbas de molho....

O mercado ficou surpreso com a decisão do Bacen de aumentar a Selic. Eu não fiquei. Alias, ontem em entrevista havia comentado que a taxa de juros deveria subir. Não, eu não tenho nenhuma bola de cristal e tão pouco acesso a informação privilegiada. O aumento é a resposta técnica ao comportamento do mercado na primeira semana pós eleição e as incertezas que devem estar presentes ate a escolha do novo Ministro da Fazenda. O Bacen tinha que enviar um sinal ao mercado, reafirmando a sua estratégia de combate a inflação. Dependendo da reação do mercado, não será nenhuma surpresa novo aumento antes do encerramento do presente ano.

A oposição reage de maneira previsivel: estelionato eleitoral, gritam a plenos pulmões e argumentam, nas redes sociais, que o Bacen teria esperado passar as eleições para aumentar a Selic: seria, portanto, uma decisão política. Pouco provável. Em que pese as pressões da atual administração sobre o Bacen, ele ainda tem um grau razoavel de autonomia e está desesperado para recuperar a credibilidade que perdeu ao longo dos últimos quatro anos. A decisão de ontem, correta do ponto de vista técnico, é um bom ponto de partida e mostra a disposição do Bacen de colocar o mercado no seu devido lugar: jogar o cambio para um nível considerado incompativel com a estratégia de combate a inflação é pedir para o Bacen jogar todo o seu peso em um hipotético quebra de braço com o mercado. O vencedor, naturalmente, seria o Bacen... É melhor o mercado colocar as barbas de molho...

A oposição reage de maneira previsivel: estelionato eleitoral, gritam a plenos pulmões e argumentam, nas redes sociais, que o Bacen teria esperado passar as eleições para aumentar a Selic: seria, portanto, uma decisão política. Pouco provável. Em que pese as pressões da atual administração sobre o Bacen, ele ainda tem um grau razoavel de autonomia e está desesperado para recuperar a credibilidade que perdeu ao longo dos últimos quatro anos. A decisão de ontem, correta do ponto de vista técnico, é um bom ponto de partida e mostra a disposição do Bacen de colocar o mercado no seu devido lugar: jogar o cambio para um nível considerado incompativel com a estratégia de combate a inflação é pedir para o Bacen jogar todo o seu peso em um hipotético quebra de braço com o mercado. O vencedor, naturalmente, seria o Bacen... É melhor o mercado colocar as barbas de molho...

quarta-feira, 29 de outubro de 2014

The French far-right mayor, the pig fest and the halal butcher

You’ve probably never heard of Hayange. It’s a town in France’s northeastern steel belt that has fallen on hard times. The Tata steel plant is still a big employer but the ArcelorMittal blast furnace shut down a few years ago.

Thanks to Fabien Engelmann, its new far-right mayor, though, Hayange is gaining lively fame, with journalists flocking there as if “on a visit to the zoo”. That’s how Mr Engelmann, who has a passion for animals and a keen admiration for the activism of Brigitte Bardot, describes the media attention.

I followed the herd to Hayange, because it’s a sort of laboratory of National Front management in a European political landscape where populist and far-right parties are causing great anxiety.

Mr Engelmann is one of more than a dozen National Front mayors elected six months ago. These mayors are supposed to demonstrate a more respectable and mainstream version of the front’s old xenophobic self.

Sadly for party leader Marine Le Pen, Mr Engelmann – a 34-year-old plumber and one-time leftist union activist before he turned far-right official – is doing a poor job at that.

Mr Engelmann comes across at first as a serious type, even when dressed in jeans and green vest. He rattles off a list of achievements: better security for a town with 15 per cent unemployment, more flowers on the streets, more festivities and no more drunken youth or aggressive beggars.

But then there is the more colourful stuff: the pig festival he staged in town, the battle with the halal butcher, the row over oriental dance and an investigation into his campaign finances. And not to forget the repainting in blue (colour of his party) of an egg-shaped sculpture that he considered “a hideous piece of art that needed refreshing”.

As you would expect, Mr Engelmann has strong views about immigration and the supposedly menacing Islamisation of French society.

His problem is the Kosovar and Albanian migrants housed in the town and living on benefits. They are, he says, a “new immigration”, families that produce five to seven children, feed off the French state and want to impose a “middle ages dogma and a religion that is not ours”. He likes the good immigrants, however: Italians and Portuguese, Serbs and Armenians who, he says, have fewer children and find jobs and housing on their own.

Mr Engelmann reassures me nonetheless that he has nothing against Muslims. In fact, the September “fête du cochon” was not meant, as I had imagined, as an affront to the Muslim refugees in town, he says. It was simply a revival of a traditional festival in Hayange, which also celebrates a national day of the sheep. Some 2,000 locals showed up to dance, listen to music and eat pork.

Mr Engelmann is a vegetarian so therefore has no preference for a specific type of meat. But he stopped a plan to serve halal meat in schools and says students will have to do with the vegetarian alternative.

Unrelated to his sentiment towards halal meat or Islam, however, is his decision to force the halal butcher in town to close on Sundays. “The halal butcher is going to lose,” declares Mr Engelmann, because he’s not a grocer and therefore is breaching the law.

After meeting Mr Engelmann, I stopped to see Abdelkader Kharchach, the halal butcher. He sells a lot of groceries in addition to meat and he has a lawyer to fend off the pressure from the mayor. He says the National Front won because people in Hayange have lost faith in politics. Many migrants have left the town since Mr Engelmann took over.

“The mayor can buy me out if he wants,” says Mr Kharchach, but he is neither closing on Sundays nor leaving Hayange.

Surely Mr Engelmann has more important things to do than pick a fight with the halal butcher.

His campaign finances are being investigated after a former deputy’s claims of irregularity. He denies any wrongdoing and professes not to be worried. This controversy is about score settling, he tells me, by a former colleague who was cast aside. And that’s because she was “a loose cannon” who alienated her colleagues.

Among her many offences, apparently, was that she would rush into his office without knocking.

Roula Khalaf

Fonte: FT

terça-feira, 28 de outubro de 2014

É preciso abandonar o mambo jambo heterodoxo...

Depois de uma eleição disputada em um cenário econômico e político claramente favorável a oposição, a atual administração conseguiu a difícil proeza de ser reconduzida ao Planalto. Foi acima de tudo uma derrota da oposição que tinha o queijo e a faca na mão, mas não conseguiu apresentar um programa crível para o eleitorado.

O desafio do segundo governo Dilma é superar os vários equívocos na condução da política econômica que foram a marca registrada do seu primeiro mandato. A indicação de um nome com grande credibilidade e amigável ao mercado para a Fazenda é um passo fundamental para reverter o quadro atual de desconfiança do mercado. Um Presidente do Bacen com reputação de aversão a inflação e com o devido pedigree acadêmico, também deveria ser parte do pacote do choque de credibilidade.

O experimento heterodoxo não apresentou o resultado prometido e por isto deveria ser deixado de lado. Uma política fiscal consistente e sem mambos jambos deveria ser a pedra fundamental de uma política econômica a serviço da construção de um país socialmente mais justo. A incompatibilidade entre a política econômica mainstream e a preocupação social é falsa.

Não é preciso reinventar a roda para traçar uma rota consistente de crescimento econômico com justiça social. É apenas necessário não confundir ideologia com política econômica: a caixa de ferramentas a disposição do policy maker é neutra e pode, portanto, ser usada para atingir diferentes objetivos. Justiça social parece ter sido o objetivo escolhido pelos eleitores, caberá a nova administraçao honrar o compromisso assumido com os seus eleitores, sem esquecer, no entanto, que a eleita, é a Presidente de todos os brasileiros.

Desejo sucesso a nova a administração.

O desafio do segundo governo Dilma é superar os vários equívocos na condução da política econômica que foram a marca registrada do seu primeiro mandato. A indicação de um nome com grande credibilidade e amigável ao mercado para a Fazenda é um passo fundamental para reverter o quadro atual de desconfiança do mercado. Um Presidente do Bacen com reputação de aversão a inflação e com o devido pedigree acadêmico, também deveria ser parte do pacote do choque de credibilidade.

O experimento heterodoxo não apresentou o resultado prometido e por isto deveria ser deixado de lado. Uma política fiscal consistente e sem mambos jambos deveria ser a pedra fundamental de uma política econômica a serviço da construção de um país socialmente mais justo. A incompatibilidade entre a política econômica mainstream e a preocupação social é falsa.

Não é preciso reinventar a roda para traçar uma rota consistente de crescimento econômico com justiça social. É apenas necessário não confundir ideologia com política econômica: a caixa de ferramentas a disposição do policy maker é neutra e pode, portanto, ser usada para atingir diferentes objetivos. Justiça social parece ter sido o objetivo escolhido pelos eleitores, caberá a nova administraçao honrar o compromisso assumido com os seus eleitores, sem esquecer, no entanto, que a eleita, é a Presidente de todos os brasileiros.

Desejo sucesso a nova a administração.

sexta-feira, 24 de outubro de 2014

Confessions of a white Oxbridge male

We straight white Oxbridge-educated males who rule Britain are used to periodic rumblings of discontent from below. Now the transvestite artist Grayson Perry, writing in the New Statesman magazine, has savaged what he calls “Default Man”: “With their colourful textile phalluses hanging round their necks, they make up an overwhelming majority in government, in boardrooms and also in the media.” The writer Caitlin Moran half-jokes that she is the only working-class Briton with a newspaper column: “I have the entire quota.”

Indeed, the Social Mobility and Child Poverty Commission notes that 59 per cent of the British cabinet, three-quarters of senior judges, half of diplomats, etc, went to Oxbridge. The typical chief executive attended Oxbridge or Harvard, says business data firm Qlik. Few of these people are women. Even those of us who groom the lower slopes of the establishment – pundits, MPs, and so forth – tend to be Oxbridge men.

My caste produces the opinions that most British people are expected to swallow. However, the one topic we seldom discuss honestly is our own rule. So let me try to describe how it looks from up here.

We didn’t have to work very hard to get here. Luckily, the British establishment doesn’t demand workaholism, except for a few months around exams. The gentleman dilettante is still honoured (see David Cameron).

Our competition to get into Oxbridge was mostly limited to other white upper-middle-class males. After that, we began recruiting each other. When I applied to the FT 20 years ago, I think I was interviewed only by white Oxbridge men, all of them straight (except for one who soon afterwards came out of the closet).

My start in journalism was unimpressive but then I didn’t have much to prove: I already was a white Oxbridge male. Aged 28, I became a columnist at another British newspaper. Perry quotes the American writer John Scalzi, who “thought that being a straight white male was like playing the computer game called Life with the difficulty setting on ‘Easy’”.

About the same time as I began work, a black friend started out at another newspaper. His news editor had little confidence in him, and my friend never got the career he wanted. Perhaps I now have his job.

We Oxbridge males help each other throughout life. Perry remarks that nobody talks about the “white middle-class community”. But it exists. Once, in a faraway land, I visited the British ambassador. Lo and behold, he was a straight white Oxbridge-educated male! He was like a friend I’d never met. He ended up giving me a briefing in his swimming pool. We Oxbridge males display exemplary class solidarity.

Our basic ideology is: trust in the system. After all, the system is run by chaps like me. I did my degree two minutes’ walk from Cameron’s college, and five minutes from the opposition leader Ed Miliband’s. I don’t identify with everyone in the establishment, because of intra-caste divides that are invisible to outsiders (for instance, Cameron is far posher than me) but the current popular rage at politicians bewilders me.

Like the communist rulers in 1989, we white Oxbridge males cannot defend our dominance with arguments. Most of us know we didn’t get here through individual brilliance. Perry is wrong when he says, “Default Man will never admit to, or be fully aware of, the tribal advantages of his identity.” I’m very aware of those advantages. That’s why, although I currently have a decent job at a good newspaper, I feel very little sense of achievement. My dad went to Cambridge. I was born to be a minor establishment functionary. That’s also why I’m not desperate for my children to join the establishment. What would it prove?

Our caste is always changing, just enough to make sure that everything stays the same. Lately we’ve learnt to lament the suffering of the disadvantaged. (I’m told that even younger members of the kleptocratic Angolan elite have mastered this rhetoric.) Indeed, many of the most stirring attacks on inequality and sexism are now produced by Oxbridge males – but then we produce most attacks on most things in Britain.

Given our podium, many of us feel a responsibility to lament our own power. But it’s hard to feel this viscerally. I believe that other people should rule. However, I’d like to hang on to my own spot. We will not make the revolution – or as the British say, turkeys don’t vote for Christmas.

We have expanded our caste a little. We now recruit some non-whites (preferably Oxbridge men). We’ve even begun admitting Oxbridge women. We just sideline them professionally the moment they make the mistake of giving birth. Still, our caste has kept raising the age at which females hit the glass ceiling: from zero, to 17 once they were allowed proper education, to 21 when we let them into Oxbridge, and now to 38. That’s progress, of sorts.

Perry warns darkly that Default Man might not rule for ever: “Things may be changing.” But I think we’ll hang on for a while yet.

Simon Kuper

Fonte: FT

quinta-feira, 23 de outubro de 2014

Commodities: A partial pump primer

Few economic forces are more important than commodity prices. When they rise they transfer riches and power from consumers to producers; when they fall, it is as near as anything in economics to a free lunch for consumers. With so much at stake, turning points are important for the global economy. Such a moment appears to be at hand.

Across a wide range of commodities, prices are falling and sometimes falling fast. The Bloomberg commodity index – which acts as a benchmark for commodity investments – fell to its lowest level in five years this week. Prices are being pushed down by the increasing supply of most commodities and a weakening global economy, including a slowing China, the world’s largest consumer for many of these raw materials. Whether it is oil, corn, iron ore, coal, cotton or copper, prices are falling quickly.

The International Monetary Fund estimates tha global commodity prices are 8.3 per cent lower than at the start of the year. In its recent World Economic Outlook report, the IMF demonstrated how a $20-a-barrel oil price decline would increase the real income of consumers, boosting domestic demand and growth in consuming countries and hitting exports and demand in producer nations. The fund estimated the net effect would increase world gross domestic product 0.5 per cent alone, and if economic confidence were improved as a result, that figure could rise to about 1.2 per cent. Gavyn Davies, chairman of Fulcrum Asset Management, says the figures were plausible and by any measure “quite big”.

Andrew Kenningham, economist at Capital Economics, has calculated that an equivalent change would transfer $640bn – or nearly 1 per cent of world GDP – from oil producers to consumers. “Our rule of thumb is that consumers typically spend half of their windfall. This is $320bn or around 0.5 per cent of world GDP, ” he says.

With other commodity prices falling alongside oil, the effects can be expected to amplify, benefiting global growth but also creating losers as well as winners. The effects are most obvious in growth forecasts. In 2011, when commodity prices were expected to remain persistently high, the IMF forecast Brazil’s economy would expand more than 4 per cent in 2014, a rate it would be able to sustain into the medium term. Now it is expecting near stagnation this year with a slow climb towards a 3 per cent medium-term rate. Russia, which also has to deal with the added impact of western sanctions, shares the same fate.

Some effects can be complicated, however. As well as redistributing money between countries, there are also winners and losers within the same nation. While falling oil prices act as a tax cut for US motorists, it hits the country’s shale oil industry. In 2011, the surge in food prices was a boon to Brazilian agriculture but a huge burden on its urban poor.

Exchange rate movements can complicate the picture, since most commodities are priced in dollars. In parts of Asia currencies are falling relative to the dollar. As a result says Jeff Currie, head of commodities research at Goldman Sachs, consumers in India are not seeing big gains because oil prices in rupees are not falling fast, and in countries such as Indonesia, the government is offsetting lower fuel prices with cuts in fuel subsidies so, again, consumers have not seen the full benefit. After taking account of currency and tax changes, Mr Currie says the US is the only country in which consumers are likely to see a big benefit.

As a big consumer and importer, the eurozone will benefit from the turndown in commodity prices, but economists warn Europe must avoid getting too much of this good thing. Falling commodity prices could tip the eurozone into outright deflation, potentially delaying consumer purchases on the expectation of even lower future prices.

This is all theoretical, but could undermine efforts by the European Central Bank to stabilise medium-term expectation of inflation to about 2 per cent a year. Thomas Harjes of Barclays says: “Market-based measures of inflation expectations are increasingly indicating that the ECB is at risk of losing its credibility to return inflation back to the close-to-2 per cent target, even over the medium term.”

● Oil: Prices driven down for motorists

Countries such as Russia, Venezuela and Iran are on edge as the price of crude oil, which has dropped sharply since mid-June, continues to struggle at about $85-$86 a barrel, writes Anjli Raval. But in countries that are net importers the price plunge has worked as a tax cut for consuming nations.

“Given that net oil consumers [advanced economies] tend to spend a higher proportion of their incomes than oil producers [notably the Gulf states but even Iran and Russia], the net impact of lower oil prices is to boost global demand,” says Andrew Kenningham, economist at Capital Economics. “That will not solve all the world’s problems, but taken in isolation it is a clear positive, not a negative.”

Forecourt prices have been slashed, even in western Europe where retail taxes rather than the wholesale cost of refined gasoline and diesel make up more than half the retail price. Falls in the price of crude take many weeks to feed through. Even so, in the UK, average petrol prices dropped to 125.4p a litre this week, a low last seen in January 2011, according to government statistics. In the US the price of a regular gallon was $3.07 this week, 15.6 per cent down from an April peak this year of $3.64.

China, the largest energy consumer in the world, is pulling back on oil demand. But falling crude prices have been a boon for Asian economies, reducing costs for businesses and consumers and giving lawmakers space to lower interest rates.

● Corn: Meat beefs up overall demand

Corn is the world’s most widely grown grain. Harvested on 180m hectares, it turns up in products from tortillas to toothpaste, writes Gregory Meyer.

The price of corn has declined by more than 15 per cent this year and is less than half of the highs reached in mid-2012. But do not expect a dash to consume more of it.

Many of the forces driving corn use are fairly static. The ethanol industry, estimated to consume a third of the crop in the US, the world’s biggest grower, has essentially reached capacity in the US as motor fuel demand holds steady. Global biofuel growth is expected to be slow.

Demand for food products concocted with the crop, such as high-fructose corn syrup and starch, is also steady.

One area where cheap corn will probably induce more consumption is in the meat industry. Enticed by high prices for steaks, bacon and chicken, livestock and poultry companies are expanding. The US agriculture department anticipates animal feed demand for corn will total 5.4bn bushels in the crop year that began last month – up more than 1bn bushels from two years ago.

“The expectation, based on history, is when you have low prices you get a response in the domestic livestock sector,” says Darrel Good, agricultural economist at the University of Illinois. There are signs this is happening: Prof Good says the numbers of chickens and milk cows is rising again in the US, while hog farmers intend to allow more sows to farrow piglets.

● Iron ore: Slowing China and oversupply dent market

Iron ore has been the standout performer in commodities this year – but for all the wrong reasons, writes Neil Hume.

The price of the key steelmaking ingredient has plunged by almost 40 per cent and recently hit a five-year low of $77.50 a tonne. Benchmark Australian iron ore for delivery into China was trading at $80 a tonne yesterday, according to The Steel Index.

The reason for the sharp fall is twofold. Vale, Rio Tinto and BHP Billiton , the big three global producers, have dramatically increased production and shipping volumes in 2014. The other big factor is slowing demand in China, which consumes about two-thirds of global seaborne iron ore.

A falling steel price will help reduce costs for many industries, including oil and gas. Steel accounts for about 30 per cent of the cost of a large oil project, according to McKinsey, the consultancy.

Ominously for the sector, more supply is set to come on stream in the coming year. BHP Billiton, the world’s largest natural resources group, estimates supply growth of 400m tonnes in the next three years, about twice its forecast level of increased demand.

Among the beneficiaries have been struggling Chinese steelmakers. They are turning to the export market because weak domestic demand has pushed prices in some local markets as low as that of cabbage.

● Cotton: Correction drives rise in consumption

The past several years have been traumatic for the cotton industry, writes Gregory Meyer.

An abrupt price rise in 2008 bankrupted some of the biggest global merchants. After another spike three years later, exasperated clothiers chose fabrics with more man-made fibre such as polyester. Cotton had a 27.5 per cent share of the global fibre market last year, from a historical norm of about 40 per cent, according to Cotton Inc, a US industry body.

Now the spindles are turning in cotton’s favour. Prices have fallen by more than 25 per cent this year to 63 cents per lb, less than a third of the 2011 peak. As China sells off a mountainous state reserve, prices are expected to remain low and steady for a long time.

The International Cotton Advisory Committee, a research group, forecasts global cotton consumption will this year rise by 3.9 per cent, well above the average annual increase.

“High prices really hurt the consumption of cotton in recent years,” says José Sette, ICAC executive director. “Now the prices are coming to more realistic levels in terms of the competitiveness of cotton with other fibres, and this would mean a recovery in consumption.”

One challenge cotton suppliers are set to face is cheaper polyester on the back of the fall in oil prices.

● Copper: Renewables sector set to benefit

Concerns about a slowdown in China’s economic growth are weighing on copper prices, pushing them down more than 9 per cent this year, writes Henry Sanderson.

Ironically the fall in price will be good for companies such as China’s State Grid which accounts for more than 80 per cent of the country’s grid investment. Its expansion plans, including an ambitious programme of new power lines, has been slowed by an anti-corruption investigation this year, yet are expected to ramp back up in 2015.

Lower prices could also help the car and renewable energy industries, which account for about 7 per cent of global copper demand, according to Metal Bulletin.

For producing countries such as Zambia and Congo, however, lower copper prices could mean a drop in fiscal revenues resulting in reduced investment and fewer jobs. This summer Zambia called in the IMF for help as prices dropped. The Democratic Republic of Congo forecasts its economy will grow by more than 10 per cent next year, though that will depend on how copper prices hold up.

The IMF said this month that a fall in prices compared with the historical average could lead to a 4 per cent reduction of real GDP in Congo this year. More than 95 per cent of its exports come from the extractive industries, mainly copper, cobalt, diamonds, gold and oil, according to the IMF.

● Coal: Lower electricity bills boost households

Coal provides about 40 per cent of the world’s electricity needs, according to the International Energy Agency, writes Neil Hume.

The funk in the market can be traced to the shale gas revolution, which has led to increased US coal exports, and growing output from the big rival exporters such as Australia and Indonesia, which have continued to churn out more volumes in spite of low prices. This has overwhelmed demand.

Analysts say India is the big growth market for thermal coal. The country has 145 gigawatts of installed coal-fired capacity and is targeting 214GW by 2020, according to Glencore, the commodities company.

In Europe, weak thermal coal prices – as well as rising solar and wind power – have left German households better off than their Dutch counterparts. Large coal-fired power plants generate more than 40 per cent of German electricity, whereas the Netherlands’ gas-fired plants account for about 70 per cent of installed capacity.

Coal for delivery into Europe within 90 days was quoted at $74 a tonne by Argus yesterday, close to a four-year low.

According to the Agency for the Co-operation of Energy Regulation, at the end of last year average German day-ahead power prices were €35 a megawatt hour compared with more than €50MW/h in the Netherlands.

Chris Giles

Fonte: FT

quarta-feira, 22 de outubro de 2014

China’s outbound investment set to eclipse inbound for first time

China’s outbound direct investment is for the first time set to exceed investment into the country, highlighting the ongoing shift of global economic influence to the east.

Outbound direct investment rose 21.6 per cent in the first nine months compared with last year to $75bn and on Wednesday a senior Chinese official said that on current trends it would probably exceed inbound investment by the end of the year.

“This is just a matter of time; if it doesn’t happen this year then it will happen in the very near future,” said Zhang Xiangchen, China’s assistant minister of commerce. “China is already a capital exporting country and it is now poised to become a net exporter of capital.”

From Africa and Latin America to the US and Europe, cash-rich Chinese investors are already snapping up real estate, companies and other assets while growth at home is poised to fall to its slowest annual pace in nearly two and a half decades.

This month a Chinese insurance company bought the iconic Waldorf Astoria Hotel in Manhattan for nearly $2bn while in the same week China’s state-owned Bright Food Group, which bought Britain’s Weetabix two years ago, took a majority stake in Italian olive oil maker Salov Group.

But with $4tn in government-administered foreign exchange reserves and Beijing’s active policy of supporting offshore acquisitions, there is enormous potential for a much larger flow of investment abroad.

The rise in outbound investment over the past decade has already been meteoric. In 2002 Chinese investors spent just $2.7bn on acquisitions and greenfield projects abroad but by 2013 the total had increased 40-fold to $108bn.

In the first half of this year there was a rare drop in outbound Chinese investment, according to alternative data published by the US think-tank the Heritage Foundation, which compiles its own numbers.

Analysts blamed the drop largely on the country’s vociferous anti-corruption campaign, which discouraged offshore deals since these are often used to skim off cash and assets and stash them beyond the reach of the Chinese authorities.

But there was a surge in deals in the third quarter, according to the Ministry of Commerce, as investment into China from abroad registered its worst performance since the depths of the financial crisis.

In July and August, investment into China dropped 14 per cent and 17 per cent respectively from the same months a year earlier.

Inbound FDI recovered somewhat in September but total investment into China of $87.4bn in the first nine months of the year was still down 1.4 per cent from the same period a year ago.

Apart from a drop during the global financial crisis, FDI inflows to China have grown steadily since the country joined the World Trade Organisation in 2001 and reached a record $118bn last year.

At current rates of growth, inbound FDI will be lucky to reach that level again this year, while outbound investment could come in at close to $130bn for 2014.

China still maintains tight restrictions on cross-border financial and portfolio investments and the renminbi is still not fully convertible, but the outward flow of direct investment is being facilitated by looser Chinese regulations.

While companies still need to consult several ministries and government agencies before they are able to invest abroad, many formal approval procedures have been simplified this year.

The Ministry of Commerce this month adopted new measures that mean it no longer approves every single outbound investment deal over $100m, although it still requires all deals to be “registered” and approvals from several other agencies are needed for most deals.

“It is expected that [the looser regulations] will further accelerate the flow of outbound capital from China, in particular into favoured markets like Australia, the US and the UK,” said Alistair Meadows, head of international capital in Asia-Pacific for JLL, the real estate investment consultancy.

The slowing domestic economy is another powerful factor pushing Chinese companies to hunt for acquisitions abroad.

The world’s second-largest economy is suffering from chronic over-investment and overcapacity after a five-year credit boom and is on track this year to post its slowest annual growth rate since 1990.

Fonte: FT

terça-feira, 21 de outubro de 2014

What is global market turbulence telling us?

The extraordinary volatility in all financial asset classes in the past week can only be described as ominous. On Wednesday, the US ten year treasury, perhaps the most liquid financial instrument in the world, traded at yields of 2.21 per cent and 1.86 per cent within a matter of hours. This type of volatility in the ultimate “risk free” asset has previously been seen only in 2008 and other extreme meltdowns, so it clearly cannot be swept under the carpet.

A few weeks ago, investors had widely expected a strengthening US economy to lead to a rising dollar and a tighter Federal Reserve, with an amazing 100 per cent of economists saying they were bearish about bonds in a Bloomberg survey in April. Instead the markets have started to act as if the world is about to topple into recession, and an abrupt reversal of speculative positions has probably led to exaggerated market moves, in both directions.

Now that excessively large positions have been washed out, what is the underlying message from the past month of market action?

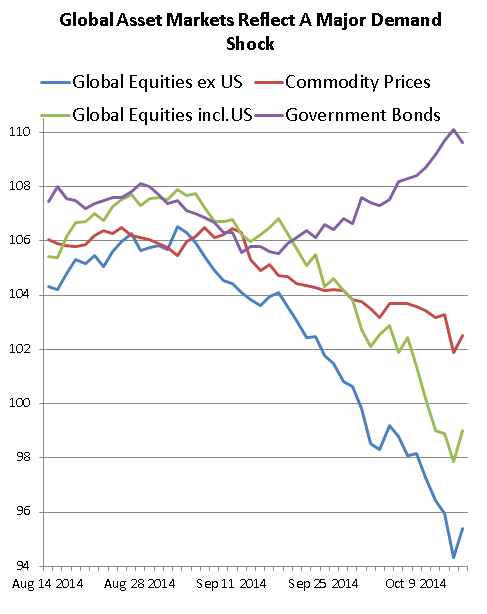

The first graph shows very clearly that the major asset classes have all moved in a classic “risk off” direction, consistent with a contractionary demand shock in the global economy – equities are down, especially outside the US, bonds are up, and commodities are down. Credit spreads have widened, including sovereign bond spreads in the euro area. Within the equity markets, cyclical stocks have under-performed, while defensives have done relatively well.

The first graph shows very clearly that the major asset classes have all moved in a classic “risk off” direction, consistent with a contractionary demand shock in the global economy – equities are down, especially outside the US, bonds are up, and commodities are down. Credit spreads have widened, including sovereign bond spreads in the euro area. Within the equity markets, cyclical stocks have under-performed, while defensives have done relatively well.

So it all seems very straightforward. Surely there must have been a sudden deterioration in economic activity. After all, the German economy has slowed markedly, taking the euro area down with it. Recent data surprises must have been adverse.

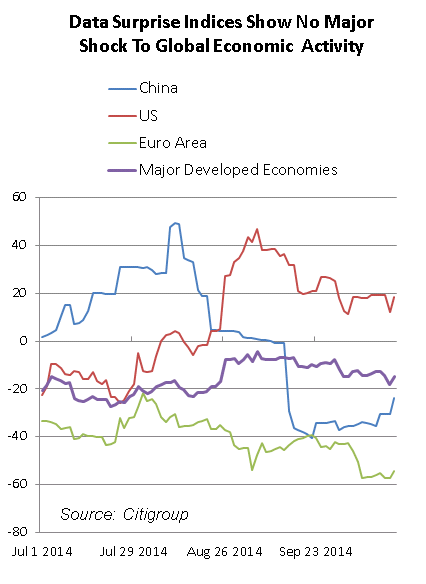

Well, no, actually. There have been downward revisions to GDP forecasts in the euro area, but these have been offset by slight upward revisions in the US and recently even in China. The latest nowcasts for global activity have remained firm, and data surprises in the world as a whole have been close to flat for several months (see graph and more details here).

Well, no, actually. There have been downward revisions to GDP forecasts in the euro area, but these have been offset by slight upward revisions in the US and recently even in China. The latest nowcasts for global activity have remained firm, and data surprises in the world as a whole have been close to flat for several months (see graph and more details here).

Maybe the slowdown in the euro area has increased the perceived risk of recessions returning to other parts of the world, but there has been no general downward revision to central projections for global GDP. In fact, J.P. Morgan’s team of economists, which tracks global activity data extremely carefully, said on Friday that signs of above trend global GDP growth were beginning to emerge. Markets have clearly been out of synch with the flow of information in this regard.

What there has been, however, is a marked drop in inflation expectations built into the bond market right across the world. This has also been led by the euro area, where inflation expectations in the inflation swap market have started to challenge the ECB’s promise to keep inflation “below but close to 2 per cent”.

Mr Draghi has said on many occasions that he will adjust monetary policy as necessary to ensure that medium term inflation expectations are in line with the ECB’s target, but investors have become hugely sceptical about this. Unless the ECB is able to alter this perception drastically in the near future, the progressive “Japanification” of the euro area could become hard to reverse.

Mr Draghi has said on many occasions that he will adjust monetary policy as necessary to ensure that medium term inflation expectations are in line with the ECB’s target, but investors have become hugely sceptical about this. Unless the ECB is able to alter this perception drastically in the near future, the progressive “Japanification” of the euro area could become hard to reverse.

So surely that must be it – declining inflation expectations, driven from events in the euro area, must have increased fears of debt deflation on a global basis.

It is hard to deny that this factor has been important. But there is also a much more benign reason for the widespread drop in inflation expectations, and that is the 25 per cent decline in oil prices since last June. Since this has been triggered largely by an increase in oil supply, it will act like a positive supply shock to oil importing economies.

In a low inflation environment, some economists may perceive even this as a bad development, since it could raise real interest rates, and may make it more difficult to service debt (see David Wessel) . But in any oil importing nation, the economy as a whole will be much better off as less resources are used to pay for oil imports, so the overall scope to service debt will improve. As long as inflation expectations remain fixed (which looks very doubtful in the euro area, but not elsewhere), the oil shock should be beneficial.

When oil prices fell sharply in 2009, global inflation went negative for a while, but inflation expectations remained stable at about 2 per cent, and no damage was done to the economic recovery. This time, real GDP is likely to benefit by about 0.5 to 1.0 per cent as a result of the oil supply shock.

Overall, then, three separate factors have probably been at work:

- a reversal of speculative positions, which has had temporary effects on asset prices;

- a contractionary and deflationary demand shock in the euro area;

- an oil shock that will also be deflationary, but will be expansionary for many economies.

The combined effects of all this should be unequivocally supportive for bonds, but ambiguous or even supportive for some global equity markets.

What am I missing? One concern is that the markets are beginning to recognise that secular stagnation may be gripping the world economy (see Robert Shiller). If so, the recent risk sell-off might have been reflecting a decline in medium term GDP growth expectations throughout the global economy. But once again this fails to show up in any recent change in consensus GDP forecasts.

Another possibility is that the market shock will itself tighten monetary conditions sufficiently to cause a slowdown in global growth, as happened in previous euro crises. But the financial system seems more robust this time, and has not shown any sign yet of increased stress.

Finally, the markets may be starting to doubt whether the central banks actually have the weapons needed to stop global deflationary forces in their tracks. Robin Harding reminds us that Ben Bernanke once said, wisely, that quantitative easing “works in practice but not in theory”. The implication is that it only works because it shifts inflation and other economic expectations in the desired direction.

If markets start to doubt this, they have entered much more dangerous waters. But the relief rally on Friday, triggered by the merest hints that central banks may consider further asset purchases, suggests that we are not there yet.

Gavyn Davies

Fonte: FT

segunda-feira, 20 de outubro de 2014

The Silver Economy: Healthier and wealthier

When Del Webb built its first retirement community in Sun City, Arizona, in 1960, the typical occupants were a retired husband and his wife who had never worked outside the home. The development promised an “active new way of life”, with a golf course, a weekly “chow night” at the recreation centre and the occasional minstrel show put on by residents.

“We would never build one like that now,” says Jacque Petroulakis of Del Webb. New developments hold fewer than 1,000 units and most have space for classrooms. Many have a motorbike clubhouse, and more than a quarter of buyers are single. “The whole idea of retirement is seen in a different light today,” says Ms Petroulakis.

The concept of retirement – and old age itself – is being reshaped by a record number of baby boomers who are, or are approaching, 65. The effects of this demographic shift are being felt well beyond Sun City.

A recent Bank of America Merrill Lynch report cites UN estimates that the number of people worldwide aged 60 years and older will double to more than 2bn by mid-century. By 2050, the number of those aged over 65 will outnumber children aged five and under for the first time in human history.

That scenario has huge implications for government, and business, not least where to find future generations of taxpaying workers.

Sarah Harper, director of the Oxford Institute of Population Ageing, says “the vast majority of people in the world will make it to age 70”, once considered extraordinary old age. The shape of the classic “population pyramid” showing large numbers of young people at the bottom with a few elderly on top has changed.

Fertility rates in developed countries, and in many emerging economies such as South Korea, have fallen so far that they face a shortage of younger workers and consumers. It means the number of those who once could be counted on to buy homes, cars, motorbikes, clothing and other consumer goods is also likely to shrink in the future.

“We’ve gone from a pyramid to a skyscraper,” Professor Harper says. “It will change the 21st century in a way we never could have imagined.”

Para ler o resto clique

sexta-feira, 17 de outubro de 2014

Ebola is turning US politics upside down

The Ebola virus has spread from Africa to the US, and that is producing noticeable changes in the American body politic. A national conversation that was weird already is growing even weirder.

The shifts are significant because Americans will be voting next month in elections that will determine the composition of the next Congress. What we talk about now could very well influence what we do later, and Ebola has transformed the current political debate.

To set the scene, it is important to remember that this was always supposed to be a good year for Republicans. Polls show they are well positioned to maintain their majority in the House of Representatives and gain control of the Senate. But the conventional wisdom held that the centrepiece of their campaign would be an all-out assault on the Affordable Care Act, or Obamacare, which has extended medical coverage to millions of Americans in the most dramatic expansion of the federal role in the health services sector in decades. The right was poised to portray the programme as yet another case of the tofu eaters in the nation’s capital sticking their noses into other people’s business.

But Ebola has turned the Republicans on their heads. Instead of blasting President Barack Obama for interfering with the US healthcare system, they are now pressing him – and federal agencies such as the Centers for Disease Control and Prevention and the National Institutes of Health – to respond more forcefully and creatively to the global epidemic.

They aren’t calling for an end to Obamacare as much as they are calling for Mr Obama to care. Pat Roberts, a Republican senator in Kansas locked in an unexpectedly tough re-election fight against an independent challenger, put it this way this week: “I call on the president to actually lead on this issue, take emergency action and protect American lives before we have an epidemic here at home.”

Republicans are suddenly asking very Democratic questions about what federal government can do to improve public health. Bloomberg News even reported that members of the appropriations committees in the Republican House and Democratic Senate are working on ways to throw more money at the problem. This would be done by increasing anti-Ebola spending in a bill aimed at keeping the government operating after December 11.

Yet the newfound Republican faith in the federal solutions has been accompanied by a hardening of hearts when it comes to the man behind Obamacare.

Conservatives are seizing on the spread of Ebola as evidence of the president’s unreliability – linking it to the advances of Islamic State militants in Syria and Iraq, management deficiencies at the Secret Service and the arrival of illegal immigrants from Mexico.

“If you look at the president’s record on anything from Isis to the Secret Service to the CDC to Syria to the border, I mean, you name it and for whatever reason, every single thing the administration, as well as these Democrats running for office, touches, it’s not turning to gold,” Reince Priebus, the Republican National Committee chairman, said this week on a Fox News talk show. “It’s turning into something else.”

The conservative critique, in some quarters, goes beyond suggestions of mere incompetence. Mr Obama is being portrayed as somehow complicit in the spread of the disease. The word “Ebola” is mutating into a metaphor for “Obama”. The two five-letter monikers roll off the tongue in much the same African-flavoured way and that seems to be enough for some folks to link them in what passes for their brains.

One of the most prominent examples of this tendency could be found recently on the Drudge Report, a widely followed website. A link to an article saying Democratic candidates were keeping their distance from the president was illustrated with an Obama 2012 campaign bumper sticker in which the word “Ebola” replaced the president’s name.

For $2.99, plus $1.49 for shipping, Amazon is offering a bumper sticker made out of “high-quality outdoor vinyl” with the same Ebola-Obama motif. Several websites have reported its appearance in California. I ran into some of the potential buyers myself on The Gateway Pundit, a self-described “leading right-of-center news website” that featured a screenshot of the Drudge Report’s Ebola-Obama image.

“A vote for Democrats is a vote for spreading disease,” said one. “Ebola gets more love than Obama – it’s certainly the less harmful unwanted African import,” added another. “Don’t forget the Obama virus, coming to your kids’ school, courtesy of legions of infectious illegals,” wrote a third. “That is already killing and paralysing our children.”

The irony is that a political leader who staked his reputation on an effort to provide health insurance to more people is now being depicted as an undercover agent of a viral apocalypse. For some of his fellow Americans, the president is less a person than a pathogen. It’s hard to avoid the conclusion that the remaining two-plus years of his term are going to be brutal.

Gary Silverman

Fonte: FT

quinta-feira, 16 de outubro de 2014

David Pilling: A weak yen is no panacea but Shinzo Abe needs it all the same

It is a truth universally acknowledged that a weak yen is good for Japan. It is a truth mostly unacknowledged – at least in Tokyo, where it is nonetheless secretly understood – that a weak currency is a vital plank of Shinzo Abe’s plans to reflate the economy. The value of the yen has fallen by about 26 per cent against the dollar since it became clear almost two years ago that Mr Abe was set to push a policy of massive monetary easing. That has helped to lift consumer prices towards the Bank of Japan’s inflation target of 2 per cent by virtue of higher import prices. There is only one hitch. A weak yen may no longer be unequivocally good for Japan after all.

There are several reasons for that. One is that Japan’s energy bill has soared as a result of closing down all 48 of its surviving nuclear reactors in the aftermath of the Fukushima disaster in 2011. That has meant importing far more oil and liquefied natural gas, often through costly long-term contracts, a blow to Japan’s balance of trade. The weak yen only makes things worse. As a result, Japan, an economy built on persistently healthy trade surpluses, has slipped into near-chronic deficits. It still records a lot of investment income from abroad, though recently this has not been sufficient to offset a widening trade gap. In August it reported a first-half current account deficit for the first time in almost 30 years.

Another reason that a weak yen may not be manna from heaven is that, contrary to common perception, Japan is no longer an export-driven economy. Exports account for about 15 per cent of output, as opposed to 51 per cent for Germany and 54 per cent for South Korea.

Many of Japan’s manufacturers, including its big car and electronics makers, have shifted production abroad to be closer to demand. More importantly, in common with many advanced countries, Japan’s service economy predominates. The bulk of Japanese are thus employed by companies that are just as likely to benefit from a stronger yen as a weaker one.

Even so, according to Capital Economics, in aggregate corporate Japan is still better off with a weaker currency. Many companies have chosen to repatriate more profits in a weaker yen than to lower prices in pursuit of higher market share. It estimates that two-fifths of Japan’s recent surge in corporate profits is attributable to a weaker currency.

That is not as good as it sounds, particularly in an economy where companies have been hoarding cash for years. Higher profits have not done much for investment. Worse, the impact on consumption has been minimal. That is because real wages have continued to fall. That may be an inevitable side effect of inflation, at least in the initial stages before higher profits are passed on in wages. As Jonathan Allum of SMBC Nikko points out, Mr Abe’s insistence on raising consumption tax by 3 percentage points probably did more damage to household spending than a falling yen.

Either way, for the prime minister – who faces important gubernatorial elections this year and local ones in the spring – it is far from ideal that most voters feel poorer because of an economic policy that bears his name.

Mr Abe is clearly having second thoughts about the virtues of a weaker yen. In remarks after the currency fell to a six-year low of Y110 against the dollar, he said there were good and bad aspects to yen depreciation. As if to underline the point, Haruhiko Kuroda, the Bank of Japan governor whose expansive monetary policy has chiselled away at the yen’s value, was summoned to parliament to explain himself.

All of this poses a dilemma for the future of Abenomics, which began by endorsing a landmark deal between the government and the Bank of Japan to co-operate in order to rid the economy of deflation. Any sign of a rift would rattle markets and weaken the credibility of a reflationary policy that relies to an uncomfortable degree on the power of rhetoric. Core consumer prices are now rising by a modest 1.1 per cent a year. It is far from clear, however, that even this is a permanent state of affairs.

As Mr Kuroda has pointed out, it is no easy matter to re-anchor inflationary expectations after 15 years of falling prices. Everyone knows that a depreciating yen is the BoJ’s most potent tool. If it is seen to falter under political pressure from Mr Abe – by, for example, shying away from another round of quantitative and qualitative easing – the whole experiment in reflation could run aground.

Mr Abe is correct in his hunch that a weak yen is no longer all it was cracked up to be. He is right too that inflation, without a compensating rise in wages, is more popular with macroeconomists than it is with voters. Yet it would be a disaster if he blinked now. Getting to sustainable inflation is the central tenet of Abenomics. A return to deflation would be to throw it all away. Like it or not, a weaker yen is part of the plan.

David Pilling

Fonte: FT

Nem todos os gatos são pardos...

Apesar de discordar da linha de política econômica, sou obrigado a reconhecer que a atual situação econômica do pais esta muito longe do quadro a la greco pintado pela oposição. Não é seguramente uma brastemp, mas seria o suficiente para, em outro pais, eleger o incumbente. Curiosamente, não é o caso no grande bananão. Ta ai um enigma a ser decifrado pelos colegas sociologos e cientistas políticos.

Um outro enigma é a resistência do candidato a uma serie de acusações em relação ao seu comportamento: suspeita em relação a drogas levantada na famosa edi ção do programa roda viva da tv cultura, a recusa em fazer o teste do bafometro no Rio, construção de aeroporto( segundo a FSP) na propriedade de um familiar que, também, controlava o seu acesso, entre outras. Se esta é uma eleição em que questões de cunho moral tem papel fundamental, porque nada disto cola na imagem do candidato da oposição.

É verdade que acusações da candidata a reeleição tem o problema da credibilidade: o eleitorado as veria como parte do jogo sujo do processo político eleitoral e, portanto, as ignoraria por completo. Mas, não é o caso da maioria das acusações que antecedem ao processo eleitoral e foram feitas por orgãos da imprensa, sabidamente, simpáticos ao candidato da oposição. Aparentemente no caso dele, vale o efeito teflon que, não se mostrou forte no caso da candidata Marina.

O histórico de comportamento moralmente questionaveis por parte do candidato da oposição, em outros países, seria o suficiente para coloca-lo fora do paréo. Aqui não parece ser importante. O motivo, me parece ser o forte discurso de odío contra a Presidente e seu Partido. É algo que ainda nos choca, mas que faz parte da vida politica em paises como os Estados Unidos e Reino Unido por ex. Ele veio pra ficar e tem o aspecto positivo de permitir a saida do armario de intelectuais conservadores que durante muito tempo foram vistos como dignos representantes do pensamento de esquerda.

Sem dúvida é uma eleição emocionante, com dois candidatos disputando cabeça a cabeça.

Um outro enigma é a resistência do candidato a uma serie de acusações em relação ao seu comportamento: suspeita em relação a drogas levantada na famosa edi ção do programa roda viva da tv cultura, a recusa em fazer o teste do bafometro no Rio, construção de aeroporto( segundo a FSP) na propriedade de um familiar que, também, controlava o seu acesso, entre outras. Se esta é uma eleição em que questões de cunho moral tem papel fundamental, porque nada disto cola na imagem do candidato da oposição.

É verdade que acusações da candidata a reeleição tem o problema da credibilidade: o eleitorado as veria como parte do jogo sujo do processo político eleitoral e, portanto, as ignoraria por completo. Mas, não é o caso da maioria das acusações que antecedem ao processo eleitoral e foram feitas por orgãos da imprensa, sabidamente, simpáticos ao candidato da oposição. Aparentemente no caso dele, vale o efeito teflon que, não se mostrou forte no caso da candidata Marina.

O histórico de comportamento moralmente questionaveis por parte do candidato da oposição, em outros países, seria o suficiente para coloca-lo fora do paréo. Aqui não parece ser importante. O motivo, me parece ser o forte discurso de odío contra a Presidente e seu Partido. É algo que ainda nos choca, mas que faz parte da vida politica em paises como os Estados Unidos e Reino Unido por ex. Ele veio pra ficar e tem o aspecto positivo de permitir a saida do armario de intelectuais conservadores que durante muito tempo foram vistos como dignos representantes do pensamento de esquerda.

Sem dúvida é uma eleição emocionante, com dois candidatos disputando cabeça a cabeça.

Assinar:

Postagens (Atom)