David Daokui Lee, an influential Chinese economist, has argued that: “The stock market sell-off is not the problem . . . the problem — not a huge one, but a problem nonetheless — is the Chinese economy itself.” I agree with both points, with one exception. The problem may prove huge.

Market turmoil is not irrelevant. It matters that Beijing has spent $200bn on a failed attempt to prop up the stock market and that foreign exchange reserves fell by $315bn in the year to July 2015. It matters, too, that a search for scapegoats is in train. These are indicators of capital flight and policymaker panic. They tell us about confidence — or the lack of it.

Nevertheless, economic performance is ultimately decisive. The important economic fact about China is its past achievements. Gross domestic product (at purchasing power parity) has risen from 3 per cent of US levels to some 25 per cent (see chart). GDP is an imperfect measure of the standard of living. But this transformation is no statistical artefact. It is visible on the ground.

The only “large”(bigger than city state) economies, without valuable natural resources, to achieve something like this since the second world war are Japan, Taiwan, South Korea and Vietnam. Yet, relative to US levels, China’s GDP per head is where South Korea’s was in the mid-1980s. South Korea’s real GDP per head has since nearly quadrupled in real terms, to reach almost 70 per cent of US levels. If China became as rich as Korea, its economy would be bigger than those of the US and Europe combined.

This is a case for long-run optimism. Against it is the caveat that “past performance is no guarantee of future performance”. Growth rates usually revert to the global mean. If China continued fast catch-up growth over the next generation it would be an extreme outlier .

In emerging economies growth tends to be marked by “discontinuities”. But what Chinese policymakers call the “new normal” is not itself such a discontinuity. They believe they have overseen a smooth slowdown from annual growth of 10 per cent to still-fast growth of 7 per cent. Is a far bigger slowdown possible? More important, would this be a temporary interruption, as in South Korea in the late 1990s crisis — or more permanent, as in Brazil in the 1980s or Japan in the 1990s?

There are at least three reasons why China’s growth might suffer a discontinuity: the current pattern is unsustainable; the debt overhang is large; and dealing with these challenges creates the risks of a sharp collapse in demand.

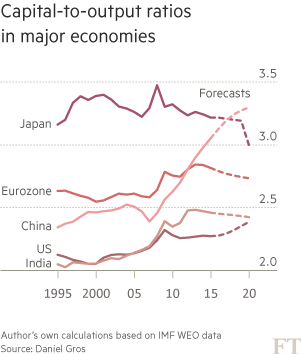

The most important fact about China’s current pattern of growth is its dependence on investment as a source of supply and demand (see charts). Since 2011 additional capital has been the sole source of extra output, with the contribution of growth of “total factor productivity” (measuring the change in output per unit of inputs) near zero. Moreover, the incremental capital output ratio, a measure of the contribution of investment to growth, has soared as returns on investment have tumbled.

The International Monetary Fund argues: “Without reforms, growth would gradually fall to around 5 per cent with steeply increasing debt.” But such a path would be unsustainable, not least because debts are already at such a high level. Thus “total social financing” — a broad credit measure — jumped from 120 per cent of GDP in 2008 to 193 per cent in 2014. The government can manage this overhang. But it must not let the build-up restart. The credit-dependent part of investment has to shrink.

The debt overhang is not the only reason why investment will wilt. Daniel Gros of the Brussels-based Centre for European Policy Studies shows that the ratio of capital to output in China is on an explosive path. Remarkably, it is already far higher than in the US. If the capital-output ratio is merely to stabilise at current levels, and the economy is to grow at about 6 per cent, the investment share in GDP needs to fall by about 10 per cent. If that were to happen suddenly, the impact on demand would cause a slump. An investment share of 35 per cent of GDP (merely back to where it was in the early 2000s) would be a desirable outcome of reforms. But moving there swiftly would take a huge bite out of today’s domestic demand.

Many believe the economy is already growing far more slowly than the government admits. But the weaker the prospective rate of growth and the more uncertain are returns, the more rational it becomes to postpone investment, further slowing the growth of the economy.

The core argument for a discontinuity is that it is hard to move smoothly from an unsustainable path. The risk is that the economy slows much faster than almost anybody now expects. The government needs to work out a way of responding that does not increase global or domestic disequilibria. The best approach would be to continue with reforms, while trying to put more spending power into the hands of consumers and investing more in public consumption and environmental improvements. Such a response would be fully in keeping with China’s needs.

A discontinuity in China’s economic growth is now more likely than for decades; such a discontinuity might not be brief; and the challenge facing policymakers is huge. They need to re-engineer a slowing economy without crashing.

Moreover, the challenge is not only, or even mainly, technical. A big question is whether a market-driven economy is compatible with the growing concentration of political power. The next stage for China’s economy is a conundrum. Its resolution will shape the world.