sexta-feira, 31 de julho de 2015

Echoes of 1989 are bad news not just for China’s markets but the world

China faces a crucial choice between the competing priorities of political control and economic liberalisation. This summer the first tremors have already been felt.

The gyrations of the Shanghai stock market — down almost a third from its mid-June high — and the exchanges in Shenzhen may seem disconnected from the real economy, since only a small proportion of Chinese and even fewer foreigners invest in them. But the market turbulence and the authorities’ response raise a fundamental question. Will the world’s second-biggest economy shift to a course that will sustain not only its own growth but also global prosperity as a whole? Or will it instead be stuck in an outmoded model in which meaningful reform is deferred because of the ruling elite’s determination to retain control? Much depends on the final decision of the Chinese Communist party, which has until now bolstered its rule with the fruits of rapid economic expansion. The significance of its choice goes far beyond China’s borders.

Some 20 months ago the party launched an ambitious programme of change, including in the financial sector. It sought to “harness the dynamism of the market” to propel China into a new stage of economic evolution, 35 years after Deng Xiaoping connected the People’s Republic with the world. But reform is not always an unalloyed blessing, especially in its early stages. It can reduce growth and cause tensions and upsets — as was the case in 1980s China.

Deng’s vision was that, after the disasters of the Mao era, growth fuelled by partial market liberalisation could make China a world power again and legitimise the unelected party leadership. That policy worked in many ways but also produced runaway inflation and corruption. It swelled criticism of the regime, leading Deng and his colleagues to send in the tanks to squash the Beijing protests of 1989. Defending party rule and maintaining its control was paramount then. So it remains.

The current leadership recognises the need for widespread economic reform. President Xi Jinping, the party’s general secretary, was the first signatory to the 60-point programme of change set out at the end of 2013. Many of the party’s elite accept it is necessary to modernise the economy, moving beyond the outdated combination of cheap labour, cheap capital and a strong export market — if only because labour and capital are no longer so cheap and foreign demand is not what it used to be.

But conservative opponents of reform can now point to this year’s turbulence in the markets as a terrible warning of the dangers of altering the system.

Meanwhile the basic political equation remains the one Deng set out in 1989: material growth in return for a political straitjacket. Mr Xi has doubled down on political control, deploying an anti-corruption campaign that has caught up many of his rivals and detaining human rights activists this summer. By contrast, he has been relatively absent from the debate on the stock market turmoil, despite his extraordinary accumulation of power, which involves him in all policy areas.

Such caution does not engender confidence that China’s most senior leader will fight hard for structural changes such as reforming the state-owned enterprises that are a source of political power. That could be bad news for Li Keqiang, the reformist prime minister and the potential fall guy for a crash.

It is a fair bet that Mr Xi would like, when he steps down in 2022, to be hailed as the leader under whom the economy reached a new cruising altitude of slower but more sustainable growth, involving higher value-added manufacturing, an expanded service sector, a switch from fixed asset investment to consumption as the main driver of the economy and reduced reliance on debt to drive expansion.

Against this rosy picture must be set the danger of being remembered as the man behind reforms that lost the party the control it has exercised sinc e 1949.

As it is, crude manipulative measures, such as pouring funds from state utilities into the markets and cracking down on share-selling, have done the rulers’ reputation no good. As in the 1980s, mandarins have had real problems in dealing with the animal spirits unleashed by liberalisation.

Today, some big international investors are taking a more leery view. Volatility has made the opening of China’s capital account look even further off. The portents are not good for Beijing’s efforts to join the International Monetary Fund’s special drawing rights currency basket, which would help make the renminbi more widely accepted. Inclusion of Chinese markets in the MSCI global index, which would be a fillip for the country’s stock exchanges, also seems problematic.

Still, such considerations will not be allowed to affect the basic calculation that reform can be pursued only so long as it does not affect the political power structure. It has to be kept under control and used, as the 2013 reform agenda put it, to strengthen the party state — not a free market.

Convulsions and official manipulation are likely to continue in Shanghai and Shenzhen. But China faces a deeper challenge in trying to reconcile the reform needed for its economy and the political control so prized by its rulers.

Jonathan Fenby is China director at Trusted Sources, a research service, and author of ‘Will China Dominate the 21st Century?’

Fonte: FT

quinta-feira, 30 de julho de 2015

Economic recoveries in Spain and Ireland accelerate

The Spanish and Irish economies are growing strongly as both recover from severe downturns to become the fastest-growing countries in the eurozone, according to the latest data.

Both Spain and Ireland were among the European countries worst hit by the global financial crisis but have made strong recoveries as a prolonged period of austerity comes to an end and consumer and business confidence returns.

Overall, the economy grew 1 per cent in the three months to the end of June, up from 0.9 per cent in the first quarter, according to preliminary figures from INE, the national statistics bureau. Official data from Dublin, delayed due to a series of extensive revisions, showed that the Irish economy grew 1.4 per cent in the first quarter.Record spending by foreign tourists helped Spain to its fastest quarter of growth since 2007, while the Irish economy has returned to its pre-crisis size and grew at six times the pace of the wider eurozone.

Tourists injected €6.5bn into the Spanish economy in June, up 4.3 per cent on the previous year. Figures for the first half of the year were also a record at €28.3bn, up 7.4 per cent from the same period in 2014, helping the Spanish economy grow for an eighth consecutive quarter.

The International Monetary Fund expects Spain’s economy to grow 3.1 per cent this year and the Irish economy to expand by 4 per cent. Earlier this week the Irish central bank, one of the most cautious of official forecasters, raised its outlook for growth both this year and next to 4.1 and 4.2 per cent respectively.

“Normality is back,” said Danny McCoy, head of Ibec, the Irish employers’ lobby. Goodbody stockbrokers calculated that the Irish economy returned to its pre-crisis level in the third quarter of last year.

Staking his re-election hopes on the improving economy, Mariano Rajoy, prime minister, has repeatedly said that reform policies put in place by his party — the centre-right Partido Popular (PP) — have been responsible for Spain’s turnround and strong economic performance.The Spanish economy is expected to play a large role in the upcoming national elections, which are scheduled to be held before the end of the year.

Last week, the INE announced that Spain had created 411,000 jobs in the last quarter, the largest quarterly growth in employment since 2005. Unemployment fell from 23.8 per cent in the first quarter to 22.4 per cent in June.

But according to José Ignacio Conde-Ruiz, a professor of economics at the Universidad Complutense de Madrid, Spain’s current growth is heavily weighted towards increases in domestic consumption.

“Better would be slightly lower growth with more investment and less consumption,” said Mr Conde-Ruiz. “Because you can’t have growth based on domestic consumption for long [periods].”

Unemployment ranks as the most important issue among Spanish voters, according to a recent survey by the national polling service. Corruption and the economy were ranked second and third respectively in last month’s survey.

Spaniards’ view of the country’s economic outlook has improved, with 28.3 per cent saying the economy would be better a year from now, compared to 15 per cent two years ago.

But the recovery may be too late and too uneven to give Mr Rajoy’s party a majority, according to Pablo Simon, editor of the political blog Politikon and a professor of political science at Madrid’s Universidad Carlos III.

Javier Díaz-Giménez, professor of economics at the IESE Business School, said: “The Q2 quarterly growth number confirms the strong performance of the Spanish economy in the first semester [half]. But growing at that rate during the second part of the year is going to be harder. The coming elections have shifted upwards the level of uncertainty and many international investors have placed Spain in a wait-and-see mode.”

Fonte: FT

Decisão esperada e correta do BC

Como esperado, o Copom aumentou a Selic para 14,25% e sinalizou o fim do ciclo do aperto monetário. Devido a alteração na meta fiscal e ao comportamento do câmbio, subir a Selic é uma decisão correta e consistente com o caminho em busca da reputação perdida por decisões equivocadas no passado, como foi o caso da redução voluntarista da taxa Selic. Já a sua manutenção no mesmo patamar por um período suficientemente longo ( três reuniões do copom, se repetir o comportamento adotado no passado) foi uma grande surpresa e é mais um indicativo da dificuldade do BC em comunicar-se com o mercado. Diria mais. É uma decisão prematura, em razão do ambiente político carregado para o próximo semestre que poderá dificultar a aprovação de medidas importantes do ajuste fiscal, alem do risco de novos gastos fruto do comportamento irresponsável de quem esqueceu que já foi governo.

Se o caldo entornar o BC ficara em uma posição constrangedora o que em nada ajudará na recuperação da sua reputação. Melhor teria sido, adotar a recomendação do Wittgenstein "sobre aquilo de que não se pode falar, deve-se calar."

Pode parecer estranho, um economista com preocupação social, como é o meu caso, defender a decisão do Copom. Na verdade, somente é uma surpresa, para quem desconhece os dados sobre a economia brasileira - herança do experimento heterodoxo da dupla Mantega-Barbosa. Manter a inflação sobre controle é o que se espera do BC e já que o lado fiscal não ajuda, cabe a politica monetária(pm) fazer o seu papel e sofrer como a Geni da velha canção do Chico Buarque.

Aos que felizmente não conheceram a experiência de viver em uma país com inflação alta e hiperinflação e os que viveram mas já se esqueceram, é sempre bom lembrar que o maior penalizado neste triste cenario macroeconômico é sempre o pobre, a população de baixa renda.

quarta-feira, 29 de julho de 2015

The rewards for working hard are too big for Keynes’s vision

If John Maynard Keynes is looking down upon me now — he might make a good guardian angel for economists — then he is wondering why I am writing this column instead of lounging by the pool.

“Three hours a day is quite enough,” he pronounced in his 1930 essay Economic Possibilities for our Grandchildren. The essay offers two famous speculations: that people in 2030 will be eight times better off than people in 1930; and that as a result we will all be working 15-hour weeks and wondering how to fill our time.

Keynes was half right. Barring some catastrophe in the next 15 years, his rosy-seeming forecasts of global growth will be an underestimate. The three-hour workday, however, remains elusive. (Keynes was childless, but NPR’s Planet Money show recently tracked down his sister’s grandchildren and asked them if they were working just 15 hours a week. They were not.)

So where did Keynes go wrong? Two answers immediately spring to mind — one noble, and one less so. The noble answer is that we rather like some kinds of work. We enjoy spending time with our colleagues, intellectual stimulation or the feeling of a job well done. The ignoble answer is that we work hard because there is no end to our desire to outspend each other.

Keynes considered both of these possibilities, but perhaps he did not take them seriously enough. He would not have been able to anticipate more recent research suggesting that the experience of being unemployed is miserable out of all proportion to its direct effect on income.

Perhaps Keynes also failed to appreciate that there is more to keeping up with the Joneses than conspicuous consumption. We want to live in pleasant areas with good schools and easy access to dynamic employers. As a result, we find ourselves in ferocious competition for a limited supply of desirable houses.

There are subtler explanations for Keynes’s error. As the late Gary Becker observed in an essay with Luis Rayo, Keynes may have been led astray by contemplating the leisured elite of the 1920s. The income flowing to the “1 per cent” was not much different back then, but they owned much more of the wealth. A gentleman in 1920s Bloomsbury drawing income from capital was just as wealthy as a partner at a 21st-century New York law firm billing at a vast hourly rate. Yet it is no mystery that the gentleman spent his time at the club while the lawyer is working her socks off.

A few years ago, the economists Mark Aguiar and Erik Hurst published a survey of how American work and leisure had evolved between 1965 and 2005. Both men and women had more leisure time — although nothing like as much as Keynes had expected. But some people defied this trend. The best educated and the highest earners, both men and women, had less free time than ever. Starting in the mid 1980s, this elite began to drop everything and work furiously.

Perhaps the real story, then, is that we are trying to keep up not with the Joneses but with our work colleagues. By pulling the longest hours and taking the least leave, we climb the corporate ladder. It may be no coincidence that the collapse in leisure time began in the 1980s, at a time when inequality at the top of that ladder was surging. The rewards for working hardest are large.

We are still 15 years away from the world that Keynes imagined. If we are to live up to his laid-back expectations, much will have to change. We’ll need plentiful access to nice schools and neighbourhoods, and less of a rat-race culture in the office.

That sounds welcome. But perhaps the fundamental truth is that many of us enjoy working hard on something that feels worthwhile, or aspire to such work. John Maynard Keynes was a wealthy man, but that did not stop him working himself to death.

Tim Harford

Fonte: FT

segunda-feira, 27 de julho de 2015

The rupture the EU needs to avoid is with Germany

The Greek crisis has put Europe in a trap. The conflict over how to solve it has eroded trust and accelerated the renationalisation of policymaking all over Europe. It has distracted politicians from the challenge of reforming Europe’s architecture and making it fit for the longer term. Meanwhile, Germany has started disengaging from the European project. Many Germans feel victimised by international criticism.

European reforms will fail if they do not address Berlin’s deepest fears. The rest of the EU must take such concerns much more seriously — starting now.

Germany’s biggest fear is that the eurozone is becoming a transfer union, with Berlin as the paymaster. Remember that Germany is the main contributor to the latest Greek bailout and has €240bn outstanding in official loans or guarantees to Greece. Demands by France and others for debt mutualisation have deepened those suspicions.

Germany’s second fear is that common European rules are circumvented all too often — as is the case with the stability and growth pact and the fiscal compact, intended to ensure debt sustainability among all members. Although Berlin itself broke the pact last decade, a strong German consensus reigns that compliance should not be a matter of discretion.

Germans reacted with disbelief when Manuel Valls, France’s prime minister, refused last year to comply with common fiscal rules, declaring: “France must be respected, it is a big country . . . We are the ones who decide on our budget.”

Germany’s third fear is that national sovereignty is being eroded without Europe delivering more stability and prosperity. Today Europe cannot credibly enforce common rules, but all members are jointly responsible for bailing out individual member states when their policies fail.

The creation of a proper fiscal union is the most urgent reform and a rare opportunity for Europe to get Germany back on board. A fiscal union should include a eurozone finance minister — an idea long favoured by Wolfgang Schäuble, Germany’s finance minister. Such a person would be accountable to a strengthened European Parliament with a new chamber for euro area issues. He or she could have the right to intervene in national budgets if these violate European law, such as the fiscal compact, and have a budget financed through a European tax as an add-on to either the value added tax or the corporate tax of euro area member states. The minister could have the ability to issue some jointly guaranteed debt within narrow limits. This ability to tax and borrow could be limited to two purposes: to provide unemployment insurance and to support investment.

A European finance minister would address all three of Germany’s fears. The EU’s boosted fiscal capacity would explicitly avoid serving as a transfer union, but operate instead a fair insurance mechanism. Member states would receive net payments in bad times — the only circumstances when debt would accumulate — but make net contributions in good times. The minister’s right to intervene in national budgets would strengthen common rules without eroding national sovereignty.

Such a post would deliver concrete benefits to EU citizens and strengthen European identity while making it harder for national politicians to blame Europe for their own failures.

The Greek crisis shows that Europe urgently needs deeper integration. Stronger solidarity should be accompanied by more shared sovereignty, as exercised by a eurozone finance minister. This would provide a mechanism to protect against recessions and crises, foster productive investment and support European workers. It would address Berlin’s deepest fears and could be common ground for France and Germany to lead Europe jointly once again.

Marcel Fratzscher is president of DIW Berlin, a think-tank

Fonte: FT

quinta-feira, 23 de julho de 2015

To boost Britain’s productivity, cancel August

The conundrum of the UK’s lagging productivity exercises some of the brightest minds in finance. There is endless talk of improved infrastructure and public sector reform. George Osborne, chancellor of the exchequer, has launched a plan aimed at closing the gap with the US. All well and good. But when it comes to the collapsing efficiency of our executives, the main problem is one that is far simpler to solve: everyone is always on holiday.

For a start, the school system is holding back corporate Britain. It is not the feckless kids accused of spending their time on Snapchat rather than acquiring basic skills. Nor is it the state sector, with its teachers blamed for being too stuck in their ways to prepare our young people for work. Instead it is the feted private school system that secures, for a handsome sum, access to the cut-throat global jobs market — and the scandal of the endless holidays that come with it.

There is a plethora of half terms, with a week or two in October, a week in February and another in May — truly an outrage, considering how short the term is. Between Christmas and the first week in January, the only emails one receives are automated holiday greetings. The Easter holidays are a good three and a half weeks, while on the continent a week is considered normal. The summer break lasts two and a half months.

Many places in Asia, the US or Europe — like the UK state system — allow children far less time off. There are a number of knock-on effects for private-school parents. First, it is much harder for mothers to work, given that they are generally the primary care-givers and that the cost of childcare in the UK as a percentage of average family income is the among the highest of all OECD countries. Second, even when a senior banker no longer has school-age children, they will assume others are off skiing/scuba diving/trekking with their offspring and will hold off making that call and doing that deal.

The fact that relationships between parents and children have grown closer over the decades also plays a part. City of London bigwigs are now proud to say they are spending time with their kids, and frequently launch unbidden into painful detail about the extra-curricular activities of their offspring.

High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/56da72fa-312b-11e5-91ac-a5e17d9b4cff.html#ixzz3glKRZzCY

Then there is “the season”. June and the first half of July are write-offs. High flyers are busy being seen at Wimbledon for the tennis, Ascot for the races, operas at Glyndebourne, classical music at the Proms, rowing at Henley. Yet again the assumption that others will be at these events leads to a drop off in productivity. The City elite, which has always complained the about month-long absences of French counterparts, now considers it normal to take August off. The phrase: “Shall we deal with this after the summer?” is now heard in June.

Big Bang, the 1986 liberalisation of the British financial system, spelt doom for old City practices such as the three-hour lunch. A burst of American-inspired power breakfasts and a long-hours culture followed. Yet the macho phrase imported from the US — “I have no time to take holidays” — died a death a few years ago. The arrival of a set of extremely rich private equity and hedge fund potentates has made confessing that you have to stay in the office into a public admission of wage slavery. The new Masters of the Universe are in charge of their destiny — and their holidays.

Having been born in Madrid but spent my working life in London, I can only smile wryly when British friends allude to “Spanish practices”. The siesta is long gone from a country that is just emerging from its worst financial crisis in a century. And, with a host of reforms passed by the present government, the nation’s impressive productivity rises could well continue.

As for the UK, there is no easy solution to its productivity puzzle. I will do my best to consider the problem. After the summer holidays.

Karina Robinson is the chief executive of Robinson Hambro, a chairman advisory firm

quarta-feira, 22 de julho de 2015

Greece is more useful to Russia inside the EU than out

We learned on Monday that Yuri Milner, the billionaire Russian entrepreneur, is to spend $100m of his own money over the next 10 years to fund a project searching for alien civilisations beyond our solar system.

According to my calculations, that is $100m more than the Russian government has offered in financial aid to Greece since the radical leftist Syriza party, often presumed to be close to Moscow, came to power in January.

During Syriza’s chaotic six months in office, the notion has cropped up time and again that Alexis Tsipras, the prime minister and party leader, would like to play a ‘Russian card’ to ward off pressure from Greece’s eurozone creditors.

There is something to this, but the picture is more subtly textured than first impressions might suggest. Let’s look below the surface and find out what’s going on.

Firstly, the contacts between the Greek government and the Kremlin have been almost entirely empty of practical results. Not a cent has found its way from Russia to Greece, and there is scant evidence that it ever will. To put it bluntly, Moscow sees the eurozone’s woes, including Greece’s debt crisis, as a European problem that Europe should pay for and solve by itself.

The Kremlin has not even exempted Greek agricultural products from the counter-sanctions imposed on the EU in retaliation for European sanctions that followed Russia’s annexation of Crimea and intervention in eastern Ukraine.

True, during a visit last month to St Petersburg, Mr Tsipras clinched a deal under which Russia promised to extend a gas pipeline project, known as Turkish Stream, from Turkey across Greek territory towards mainland Europe. But this project is still a long way from taking concrete form. All in all, you would have to say that Russia exerts more influence in certain former communist allies in the Balkans than it does in Greece.

Secondly, it is clear that Russian policymakers such as Anton Siluanov, finance minister, oppose Grexit – Greece’s exit from the eurozone – and want the country to stay in Europe’s currency union and the EU. For Grexit might trigger financial market turmoil that would be highly unwelcome for Russia, which is battling an economic downturn exacerbated by low world energy prices and western sanctions.

From a diplomatic point of view, a friendly Greece is more useful to Russia inside the EU, where it can put forward arguments that chime with Moscow’s interests, than outside.

Thirdly, whatever Mr Tsipras and his Syriza colleagues imagined in their naïveté six months ago, I suspect it has dawned on them by now that Russia is not going to be their financial or diplomatic saviour. To be clear, this has not stopped Mr Tsipras from playing the ‘Russian card’ – but he has done so in a way that resembles a conjuring trick more than a genuine ace in the deck.

The best example came immediately after Greece’s July 5 referendum, in which voters backed Mr Tsipras’s opposition to rescue conditions laid out by the creditors. From the prime minister’s office in Athens emerged smoke signals that he was in touch with the Kremlin, seeking support from President Vladimir Putin to help him in his resistance to other eurozone governments.

The central point here is that he wasn’t trying to wangle money out of Mr Putin, let alone planning to abandon the west for Russia. Instead, he was attempting to create an illusion that he was up to something unsettling for Greece’s western allies.

At one level, he was trying to prompt the Obama administration, which was already nervous about the geopolitical implications of the mishandling of the Greek problem, into putting more pressure on the Europeans not to let Greece drop out of the eurozone.

At another level, his supposed courtship of Russia was an attempt to win the attention of German Chancellor Angela Merkel, who is widely viewed as more alert than Wolfgang Schäuble, her finance minister, to the geopolitical risks of Grexit.

In a limited sense, Mr Tsipras’s gambit worked, but at a very high price. The US did indeed exert pressure to prevent Grexit, and Germany decided to give Greece another chance in the eurozone. But Mr Tsipras has been compelled to embrace an exceptionally tough aid-for-reform programme that goes against everything he and his party stand for.

What started as playing a Russian card has ended up as Russian roulette.

Tony Barber

Fonte: FT

terça-feira, 21 de julho de 2015

Let China’s markets speak truth to power

Recent turbulence in China’s stock market has led some to conclude that the country stands on the brink of a major financial and economic crisis. The rapid decline of equity prices, these bears maintain, is a warning of contagion to come.

While it is no secret the Chinese economy faces significant challenges and headwinds, these have little to do with the sell-off in the stock market. Rather, they stem from underlying structural problems, including unfinished reforms to China’s capital markets. All equity markets are prone to boom and bust cycles. Problems arise when capital markets are under-developed — as they are in China — because these bouts of volatility are magnified.

China is especially vulnerable at this point because while its economy has grown and matured, its capital markets have lagged behind. It is no surprise that those ideologically opposed to markets would use recent events to make the opposite argument — that to prevent market instability, Beijing should slow the pace of financial liberalisation or perhaps even abandon market-based reforms altogether.

With so many retail investors in China’s stock market, a collapse of share prices affects people’s savings, incomes and welfare. Many no doubt invested because they were confident in the government’s capacity to rescue the market. This may explain, in part, why Beijing intervened so quickly when the market plummeted. Still, while Beijing’s instinct to protect investors is understandable, the best way of doing so is to create a modern capital market.

No advanced economy has achieved high-income status — something to which China aspires — with a closed financial system that misallocates and misprices capital. Chinese reformers undoubtedly understand how to create a modern financial system; policymakers have studied this inside out. They have the blueprint in hand, but need to act on it boldly and quickly. If China is to have a well functioning and stable capital market — which can also help to protect investors, particularly unsophisticated individuals — it needs to allow best-in-class financial institutions and professionals, irrespective of national origin, to serve Chinese investors. In my experience, joint ventures simply do not work for global financial institutions.

China would do well to allow a wide range of participants, including top-notch foreign institutional investors, investment banks and brokers, to compete on equal footing. Exposing companies to serious competition will sort out the best institutions from underperforming ones. Beijing can further protect investors by establishing a well enforced regulatory regime designed to minimise accounting fraud and market manipulation, ensure high quality investment products, set appropriate margin requirements, and mandate high standards for the sales practices of brokers that sell to individuals.

Investors also need to be able to diversify their assets. This is one of the reasons Beijing should establish a more robust domestic corporate bond market, and allow the Chinese public to invest more of their assets in foreign securities. Beijing also needs to do more to ensure a healthy market ecosystem, including transparent accounting and disclosure standards and the presence of professional equity research firms and independent debt rating agencies.

Finally, for public equity offerings, China should move away from a registration system that depends on central government approval. Rather than being the “gate keeper”, the government should simply set appropriately high standards and criteria for companies seeking to go public, thereby depoliticising the process and letting the market be the decisive force.

Recent market tremors have led to some scapegoating of foreign speculators. This volatility should be seen instead for what it is: a sign that financial reforms have yet to be fully realised.

Keeping the present halfway house will make it harder for China to avoid the middle-income trap that has kept many emerging markets from becoming a prosperous economy. Indeed, top Chinese policymakers know they must expend greater energy to execute the reform agenda President Xi Jinping laid out 20 months ago.

For nearly four decades, China has reformed by following Deng Xiaoping’s dictum to “cross the river by feeling for stones”. It is time to more boldly cross the river to reach the other shore.

Henry Paulson, a former US Treasury secretary and chief executive of Goldman Sachs, chairs the Paulson Institute

Fonte: FT

quinta-feira, 16 de julho de 2015

Delors had the answer to the Greek question

There is a well-worn aphorism heard among British politicians that says the way to keep a secret is to announce it in the House of Commons. Something similar is true of Europe. This week’s deal to keep Greece in the euro leaves two questions: will it work; and what can be done to strengthen Europe’s monetary union. Sad to say, the answer to the first is “probably not”; as for the secret formula that would secure the future of the euro, it was published 25-odd years ago.

The obvious observation on the latest bailout plan is that its harsh terms were at once inevitable and potentially counter-productive. There can be no argument that Greece requires radical reform. This has nothing to do with whether it stays in the single currency or returns to the drachma. Dismantling clientelism and collecting taxes are prerequisites for Greece to become a modern, functioning democracy. The big danger of so-called Grexit is that the impetus for change would evaporate. Greece’s future would be as Europe’s Venezuela — only without the oil.

What is also true is that the creditors — and above all Germany — have allowed their explicable anger and frustration with the antics of Alexis Tsipras’s Syriza government to cloud their judgment about the shape of a new agreement. The International Monetary Fund’s latest evaluation of Greece’s dire economic predicament told us what we knew: whichever way you cut it, Athens needs a sizeable debt writedown.

The word in Berlin is that this is a problem for the long term. The immediate debt-servicing burden is relatively light. This is to ignore political psychology. The Greek people need incentives to embrace change — light at the end of the tunnel, as the cliché has it. The chances of Athens sticking rigorously to a new programme were always going to be fairly slight. Without the promise of debt relief they vanish.

As negotiations get under way in the coming weeks, creditors should also be flexible about short-term fiscal targets. You do not have to be a paid-up Keynesian to believe austerity can be counter-productive. There should be a trade-off with structural reforms. The more Athens does to clean up governance and allow markets to work, the less fixated creditors should be on the precise size of its primary surplus.

Ah, I hear politicians in Berlin say, but what about Chancellor Angela Merkel’s problems with the Bundestag? Her party will not accept any concessions. The answer is straightforward. If Ms Merkel wants to keep the euro afloat then Germany too has to own up to reality. Leaders sometimes have to spend accumulated political capital. Or does Ms Merkel want to be remembered as the author of the fracture of Europe?

Whatever the outcome of the negotiations — and I admit it is hard to be optimistic — deeper doubts about the future of the euro remain. Sure, Anglo-Saxon economists have been predicting its imminent demise for the past five years and have been wrong on every occasion — mostly because they have not paid attention to politics. But to rescue the single currency is one thing; to underwrite its long-term future another.

For now, the euro is stranded in no-man’s-land. Perhaps that is why smart officials in Berlin have been rereading the report produced in April 1989 by a committee of central bankers and eminent experts. Chaired by Jacques Delors, then president of the European Commission, the committee was charged with producing the blueprint for a single currency. Its Report on Economic and Monetary Union in the European Community did just that.

Among the authors of the Delors report there were doubts much would come of it. As an economics writer for the Financial Times, I was counselled by senior figures in Frankfurt not to pay much attention to the plan, even though Karl Otto Pöhl, then president of the Bundesbank, was a prominent signatory. Germans, I heard, would never consent to give up the Deutschmark.

The authors, though, could not have predicted that six months later the Berlin Wall would come down, transforming the political dynamics of European integration. Germany’s Helmut Kohl got German reunification and François Mitterrand, the French president, secured economic and monetary union.

Except that this last sentence is not quite right. What was agreed at Maastricht two years later was monetary union. The “economic” bit was dropped, because France, among others, was jealous of its national sovereignty.

By opting for a strictly monetary union, EU leaders sidestepped the core tension that still torments the euro. Where does the balance lie between solidarity — a eurozone budget and transfers from rich to poorer nations — and the collective responsibility of mutually binding economic and fiscal rules?

The committee foresaw that the eurozone could never be modelled on the US. European nations would never pool sufficient sovereignty. But the report emphasised that economic union demanded serious constraints on national decision-making and, at times of stress, official resource transfers: responsibility and solidarity, in other words, would sit side by side.

Critically, the committee concluded: “Economic and monetary union form two integral parts of a single whole and would therefore have to be implemented in parallel.” They never were, and that was the big mistake. The euro will be safe only when it is rectified.

Philip Stephens

Fonte: FT

quarta-feira, 15 de julho de 2015

The end of an affair for France and Germany

European integration is a game that involves up to 28 players and at the end the Franco-Germans win. So it has been for close to 70 years, and so it was again in Brussels last Monday with Angela Merkel and François Hollande setting the terms of a deal subsequently blessed by all others. This may have come as a surprise, given the huge differences between the two countries’ positions. The Franco-German system was being tested to the limit.

The often-forgotten secret is that France and Germany rule the roost not because they agree but because they do not: De Gaulle wanted a Europe of nation states, Adenauer was a self-avowed

federalist, and a few days ago Berlin was actively considering Grexit, while Paris worked to keep Greece in the single currency. Because the two countries often represent polar opposites within the mainstream EU conversation, a deal struck by Germany and France can usually be accepted by all, minus the UK. This does not mean the couple’s balance remains unchanged. During the cold war, a strategically dependent Germany ceded the central role to France. Nowadays, German leadership on issues such as Ukraine is made acceptable thanks to cover provided by France. Similarly, the deal struck in Brussels on Greece bears the “no-debt-forgiveness” footprint dear to Germany.

Last Monday, France was one of only three countries out of 18 ready to sign on to a new bailout deal with Greece (Italy and Cyprus were the two others). But it is France and Germany together who took the final decision. Germany kept debt restructuring off the table. France

also got what it wanted: no Grexit. Mr Hollande received high acclaim on his return from Brussels.

So the tired old couple still works some of its magic. The fact Ms Merkel and Mr Hollande share character traits may have helped: unabrasive and diffident, they are born proponents of the quest for compromise, important in German coalition-building and the Socialist party’s art of synthesis.

However, this could be a last fling, as the faultlines that opened last week deepen and widen. By openly contemplating the forced secession of Greece, Germany has demonstrated that economics trump political and strategic considerations. France views the order of factors differently, as is clear in Mr Hollande’s July 14 proposal to make the eurozone a politically accountable body with its own parliament and budget. This could still be fudged if the new bailout scheme were successful.

Unfortunately, by having avoided what they loathe — debt forgiveness — the Germans may now be hoist with their own petard. Adding billions to Greek debt, enforcing pro-cyclical pension cuts and tax increases in the middle of renewed recession, and positing as in 2011 a !50bn privatisation programme: this is as unlikely to work now as it was in the past. Now it has acquired the formal status of plan B, Grexit is likely to come back. France would then be faced with an impossible choice: to flow with the German-led tide of Grexit, clearly as a subordinate, or to fight a losing battle to prevent a country from being forced out of the European family.

Even Franco-German co-management may not be up to striking a workable compromise. The change behind the scenes is that the Paris-Berlin bond can no longer take strength from the shared project of European integration: France’s 2005 rejection of the proposed EU constitution was a turning point. The relationship has instead become utilitarian and as a result the EU’s days of ever closer union may be at an end.

François Heisbourg is special adviser at the Paris-based Fondation pour la Recherche Stratégique

Fonte: FT

terça-feira, 14 de julho de 2015

Imperial ambitions have pushed Europe to its limits

A few years ago, I heard an after-dinner speech from a European statesman, a person who has played a leading role not only in the political life of his own country but in the councils of the EU. The speaker that evening lauded, to general agreement, Europe’s values — its culture, its solidarity — and the quality of its institutions. He went on to stress the need for the union to propagate these values and institutions more widely.

The discomfiture I felt was shared by some of those sitting with me at the table. My problem was that I could have put similar words into the mouths of some of the most unpleasant figures in world history. The EU that the speaker described was an imperialist project. Those who proclaimed the British empire used to sing: “Wider still, and wider, may thy bounds be set. God who made thee mighty, make thee mightier yet.” Britons may still sing “Land of Hope and Glory” but they no longer take the words seriously. Yet the expansion of the EU embraced a similar vision.

For the builders of modern Europe, wider union has been as important as closer union. Greece was hastily admitted in the hope of sustaining its fragile democracy after the end of military rule; Spain and Portugal followed soon after. Every post-communist state with passably honest and democratic institutions, and some without, has secured admission. The ambitious project of creating monetary union between France and Germany was extended, by lowering admission standards, to include most EU members. The principal qualification for membership of a European club has been the desire to join.

Of course, there are big differences between the Europe of the 21st century and the empires of the 19th and 20th: notably, traditional imperialists did not seek the consent of those they colonised and they suppressed most forms of democratic expression. Yet Greeks today might not perceive these differences as being particularly large.

So the question is whether, like so many imperialist projects throughout history, the European project has stretched its territorial boundaries beyond the limits it can plausibly sustain. That question is highlighted by the two existential problems the EU faces today: the geopolitical confrontation with Russia, and the troubled relationship between peripheral economies and the eurozone.

The boundaries of western Europe have been pushed as far east as at any time in history, save for the best forgotten precedent of the Nazi occupation of most of the continent in 1941-42. The Ukraine crisis tests how far implied promises of political, economic and ultimately military support in that extension will be maintained when called on. The Baltic states have reasonable cause to feel nervous about the solidity of the commitment of their new allies.

Few people can now doubt that it was a mistake to let Greece join the euro in the first place. And this is not just a matter of economics — the fudged data, profligate spending and unpayable debts. The central Greek problem is that the country’s political institutions are not sufficiently mature to effect competent administration or economic management, or to engage in a responsible manner with the institutions of western Europe. And Greece is not the only member state of the EU to which that critique could be applied.

The empires of history have generally collapsed from overstretch, which led to restive populations on the peripheries, and then to doubts about the wisdom of the project in the home country itself. These symptoms are recognisable in Europe today. The EU has achieved its successes by always pushing integration a little further and faster than its institutions would easily support or its populations readily accept. Perhaps that ambitious strategy has now been taken a step too far.

John Kay

Fonte: FT

segunda-feira, 13 de julho de 2015

Greece’s brutal creditors have demolished the eurozone project

A few things that many of us took for granted, and that some of us believed in, ended in a single weekend. By forcing Alexis Tsipras into a humiliating defeat, Greece’s creditors have done a lot more than bring about regime change in Greece or endanger its relations with the eurozone. They have destroyed the eurozone as we know it and demolished the idea of a monetary union as a step towards a democratic political union.

In doing so they reverted to the nationalist European power struggles of the 19th and early 20th century. They demoted the eurozone into a toxic fixed exchange-rate system, with a shared single currency, run in the interests of Germany, held together by the threat of absolute destitution for those who challenge the prevailing order. The best thing that can be said of the weekend is the brutal honesty of those perpetrating this regime change.

nor even the total capitulation of Greece. The material shift is that Germany has formally proposed an exit mechanism. On Saturday, Wolfgang Schäuble, finance minister, insisted on a time-limited exit — a “timeout” as he called it.

I have heard quite a few crazy proposals in my time, and this one is right up there. A member state pushed for the expulsion of another. This was the real coup over the weekend: not only regime change in Greece, but also regime change in the eurozone.

The fact that a formal Grexit may have been avoided for the moment is immaterial. Grexit will be back on the table when you have the slightest political accident — and there are still many things that could go wrong, both in Greece and in other eurozone parliaments. Any other country that in future might challenge German economic orthodoxy will face similar problems.

This brings us back to a more toxic version of the old exchange-rate mechanism of the 1990s that left countries trapped in a system run primarily for the benefit of Germany, which led to the exit of the British pound and the temporary departure of the Italian lira. What was left was a coalition of countries willing to adjust their economies to Germany’s. Britain had to leave because it was not.

What should the Greeks do now? Forget for a moment the economic debate of the past few months, over issues such as the impact of austerity or economic reforms on growth. Instead ask yourself this simple question: do you really think that an economic reform programme, for which a government has no political mandate, which has been explicitly rejected in a referendum, that has been forced through by sheer political blackmail, can conceivably work?

The implications for the rest of the eurozone are at least as troubling. We will soon be asking ourselves whether this new eurozone, in which the strong push around the weak, can be sustainable. Previously, the strongest argument against any forecasts of break-up has been the strong political commitment of all its members. If you ask Italians why they are in the eurozone, few have ever pointed to the economic benefits. They wanted to be part of the most ambitious project of European integration undertaken so far.

But if you take away the political aspiration, you may end up with a different judgment. From a pure economic point of view, we know that the euro has worked well for Germany. It worked moderately well for The Netherlands and Austria, although it produced quite a degree of financial instability in both.

But for Italy, it has been an unmitigated economic disaster. The country has seen virtually no productivity growth since the start of the euro in 1999. If you want to blame the lack of structural reforms, then you have to explain how Italy managed decent growth rates before then. Can we be sure that a majority of Italians will support the single currency in three years’ time?

The euro has not worked out for Finland either. While the country is considered the world champion of structural reforms, its economy has slumped ever since Nokia lost the plot as the world’s erstwhile premier mobile phone maker. Whether the euro is sustainable for Spain and Portugal is not clear. France has performed relatively well during the euro’s early years, but it, too, is now running persistent current account deficits. It is not only Greece where the euro is not optimal.

Once you strip the eurozone of any ambitions for a political and economic union, it changes into a utilitarian project in which member states will coldly weigh the benefits and costs, just as Britain is currently assessing the relative advantages or disadvantages of EU membership. In such a system, someone, somewhere, will want to leave sometime. And the strong political commitment to save it will no longer be there either.

Wolfgang Münchau

Fonte: FT

sexta-feira, 10 de julho de 2015

Germany’s Failure of Vision

The Greek crisis represents the first real test of German leadership since World War II. Chancellor Angela Merkel of Germany has thus far flunked it, with tragic consequences for Europe.

After the fall of the Berlin Wall, leadership of Europe was firmly in French hands. With Germany preoccupied by reunification, Jacques Delors, then the president of the European Commission, was the moving force behind the Maastricht Treaty, which transformed the common market into a more powerful European Union. With the dawning of the new century, the former French president Valéry Giscard d’Estaing, inspired by the Philadelphia convention of 1787, was chairman of a convention in Brussels that proposed a constitution to enhance the power and legitimacy of the European Union. But French voters (of all people) rejected this initiative in 2005. Since then, European elites have been enhancing their power through treaties and agreements that did not require popular ratification.

Ms. Merkel once joined with President Nicolas Sarkozy of France in leading the European project. But France’s economic decline, and the political weakness of Mr. Sarkozy’s successor, François Hollande, has propelled her onto center stage.

Even a decade in, her inexperience shows. For starters, she has treated the debt crisis narrowly, as an economic problem, failing to consider Greece’s role in defending Eastern Europe against a resurgent Russia. This failure is remarkable, since it was only last February that she went to Minsk, Belarus, to negotiate with President Vladimir V. Putin of Russia on a Ukraine cease-fire.

America was largely on the sidelines, astonishing for a matter of war and peace on the Continent.

It is hardly surprising that President Obama called on Ms. Merkel to show flexibility in the debt crisis, given Greece’s critical geostrategic role in NATO. The issue goes far beyond the leftist Syriza party’s flirtation with Mr. Putin as a counterweight to European technocrats in Brussels, Strasbourg and Frankfurt. It is in Germany’s paramount interest to keep the eastern frontier of Europe as far east as possible. The United States is already overextended in the Middle East and in East Asia. If Germany is to deter Russia effectively, it must gain the continuing cooperation of Greece and other NATO allies, like the Baltic countries, that because of proximity are potentially in the line of fire. But instead of heeding Mr. Obama, Ms. Merkel chose the path of humiliation.

Syriza’s bargaining tactics have been erratic, but there was nothing inappropriate about its call for a referendum. If Prime Minister Alexis Tsipras was considering backtracking from key campaign promises, it was only right for him to consult voters at this crucial turning point. To encourage sober deliberation, Ms. Merkel should have urged the European Central Bank to keep Greek banks open during the run-up to the referendum. But the Eurocrats did the opposite, using brute force — choking off the flow of cash — to impress Greece’s vulnerability on its voters. Moreover, the bailout offer expired, so confused voters weren’t even sure what, exactly, they were deciding.

At this point, the International Monetary Fund intervened in a way that could have decisively transformed debate. Last Thursday, it offered the first serious long-range plan for a Greek recovery. In exchange for serious reforms from the Tsipras government, the I.M.F. dangled the possibility of substantial debt forgiveness and emergency loans.

The I.M.F. shift was headline news, since the I.M.F. had been a driving force behind the austerity program for five years. With Mr. Tsipras himself cheering the I.M.F.’s agonizing reappraisal, a positive response from Ms. Merkel might have served to rally the “yes” vote.

But Ms. Merkel instead gave the I.M.F. the silent treatment, allowing Syriza to convince Greeks that a “no” vote was the only way to break out of the austerity trap. They rejected Europe’s bullying.

Ms. Merkel is by no means an innocent bystander to this mess, but it’s not too late for the chancellor to undo her mistake. As negotiations move into the do-or-die phase, she should encourage the I.M.F. to mediate the increasingly bitter dispute. The fund is the only institution that has earned credibility from both sides. Its long-term plan provides the only serious framework that promises to minimize creditor losses and maximize Greek prospects. Ms. Merkel should also urge the European Central Bank to renew emergency funds so that normal financial and banking operations may resume.

This strategy promises something more than an economic breakthrough. It represents Germany’s last, best hope for avoiding a catastrophic re-entry as the unquestioned power on the Continent. Preventing the consolidation of such power in a single country (and in a single leader) was one aim of the European Union’s architects. Will Ms. Merkel have the courage and wisdom to defend their vision?

Bruce Ackerman, a professor of law and political science at Yale, was a spring fellow at the American Academy in Berlin.

Fonte: N Y Times

quinta-feira, 9 de julho de 2015

Europe must remember that this crisis is not Greece alone’s

As the debate over Greece’s membership of the euro lurches towards its final act, there is a rising risk that this very European crisis is seen in overwhelmingly national terms.

This is true in Germany, which will play a crucial role in resolving the dilemma, as it is elsewhere in the bloc. But Europe’s leaders and people must rise above this temptation, despite all the frustrations of the Greek saga.

Many Germans firmly hoped that last weekend’s referendum would deliver a Yes.It would have been taken as a strong signal that Athens still sees the euro as a vital means of modernisation. But Greece saw things differently. Its No vote united German public debate as rarely before.

While previously Athens’ stubborn position was mostly attributed to the Syriza government, the No vote made clear it had popular backing.

The great majority of the German parliament would clearly prefer Greece to remain in the eurozone — but on condition that the country be ready to modernise by establishing a functioning state and efficient economy.

This willingness is in doubt. Should the Greek government fail to dispel these doubts, a new aid package would cause a devastating loss of credibility for the euro and the EU as a whole. And yet, if Grexit does indeed occur, such modernisation will become even more difficult. This is part of the Greek dilemma.

There is still hope that these two extremes can be avoided. If the Greek government proved able to present a viable reform plan, a stormy debate could ensue but the German parliament would ultimately be likely to vote to support for its European partner.

However, even if an EU-Greece deal is reached on Sunday, it will only be a temporary fix to a problem that runs much deeper than the current crisis. Indeed, what we are seeing is first and foremost a European crisis — economic, geopolitical and political in nature. Greece is just part of it.

A failure of the common currency in Greece would make the eurozone as a whole much more vulnerable,since markets would challenge other European economies. Although the eurozone has become more robust since the financial and economic crisis first hit in 2007-2008, it is still lacking sufficient resilience to withstand external shocks.

Grexit and all the ensuing doubts about Athens’ European future would also thwart the EU’s efforts to combat threats in the continent’s east and south.

All this has to be seen in the context of the deepest European political crisis since the Treaty of Rome. A rise in self-interested nationalism — a phenomenon of which Syriza is part — is leading to a general paralysis in European decision-making. The ineffective response at the last European summit to the refugee crisisshowed as much.

High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/b1cf5560-23ff-11e5-bd83-71cb60e8f08c.html#ixzz3fRO7hZJB

This is the challenge for the EU as a whole. Do we continue with what amounts to a laissez faire attitude, in which narrow nationalism extends an ever-tighter grip on member states; or instead forge a true European leadership that recognises our most urgent problems not as national but as European problems? Problems such as persistently high unemployment — particularly among the young — are undermining governments’ democratic legitimacy. No less important challenges are the refugee crisis and the question of how to guarantee European security in the 21st century.

Governments must not only speak to their electorates in national terms but also take up the burden of explaining unpopular decisions when necessary. Germany, like other European member states, has a strong interest in solving this crisis: the euro and Europe are the most important foundation of our economic and political stability. We simply cannot afford to concern ourselves merely with our respective national interests. All European member states can flourish only in a stable EU. Therefore, we need a European success — a European deal that looks beyond ideological trenches and blends liberal reform efforts with policies that stimulate jobs and growth.

All this will come at a cost. Yet not solving these problems would be much more expensive, both economically and politically. Even the more prosperous of the European countries will not continue to do so well if other member states are suffering. Today, there are no longer purely national costs and benefits but only European ones.

Norbert Röttgen is chairman of the Bundestag’s foreign affairs committee

Fonte: FT

quarta-feira, 8 de julho de 2015

Lew and Lagarde raise pressure on EU to avoid Grexit

US Treasury secretary Jack Lew and the IMF’s Christine Lagarde on Wednesday sought to increase pressure on European leaders to grant debt relief to Greece and help the country avoid an exit from the eurozone.

In separate interventions in Washington both said it was clear that Greece was in need of a “debt restructuring” in an implicit call for Germany and others to drop their opposition to any forgiveness of Greek debts.

“Greece is in a situation of acute crisis, which needs to be addressed seriously and promptly,” Ms Lagarde said. Getting out of that crisis would take both reforms by Athens and a “debt restructuring”, she said.

Warning that a Greek meltdown would cause hundreds of billions of dollars of economic damage around the world, Jack Lew issued the Obama administration’s loudest call yet for compromise.

Athens needed to play its part by giving the rest of Europe confidence that it would fulfil a new set of reform pledges, he said. But he also called on European creditors to be ready to restructure Greece’s €317bn debt pile.

“In the next few days what we’ll see is [whether] the parties come together and build enough trust that Greece will take the actions that it needs to take so that Europe will restructure the debt in a way that is more sustainable,” Mr Lew said.

“I certainly have ideas about how you can do that,” he added. “But it’s . . . a lot to do in a short period of time and I’ve said over and over again that the risk of an accident goes up dramatically when you create more of these kind of life and death deadlines.”

US officials have in recent weeks gradually been raising the pressure on both Greece and creditors such as Germany and France to come to a deal and steer around what many in Washington see as an avoidable crisis.

President Barack Obama spoke with both Angela Merkel, the German chancellor, and Alexis Tsipras, the Greek prime minister, on Tuesday. Mr Lew and other officials have also been in regular contact in recent days with their counterparts across Europe and at the International Monetary Fund.

The US has become an important advocate for granting Greece debt relief. Washington backed an IMF decision last week to release a controversial debt sustainability analysis that argued forcefully for a restructuring.

Ms Lagarde on Wednesday defended the release of that report just days ahead of Sunday’s referendum in Greece, saying it had never been intended to be a political move. Both sides in the referendum had seized on the report to their own ends, she pointed out, and it had simply enumerated what had been a longstanding IMF call for Greece’s debts to be restructured.

“Our analysis has not changed,” she said.

Mr Lew said the Greek crisis did not pose “any immediate threat” to the US economy.

But, speaking at a Brookings Institution event in Washington, Mr Lew lamented that Greek and European leaders had previously been within “a couple of billion dollars” of reaching a deal but were now creating economic risks on a far larger scale in Europe and beyond.

“For any of us who have participated in budget and fiscal policy discussions, you wouldn’t usually buy hundreds of billions [of dollars] of risk for a couple of billion dollar gap,” Mr Lew said.

“There’s a lot of unknowns if this goes to a place that completely melts down in Greece. I think that is a risk that the Europeans and global economy don’t need. I think geopolitically it would be a mistake.”

Mr Lew said the Greek prime minister could not accept new fiscal and structural reforms without being able to show voters that the country’s debt would be sustainable, and that no European government could support a deal without assurances that it would be properly implemented.

Fonte: FT

terça-feira, 7 de julho de 2015

Grexit will leave the euro fragile

So what should the eurozone do now? Last week I concluded that the Greeks should vote Yes. They decided instead overwhelmingly to reject the terms of a deal that had been withdrawn. What might that mean? And how should the eurozone respond?

Apparently many, perhaps most, of those who voted believe their rejection would force a change of heart in the rest of the eurozone. Their partners would come to recognise the error of their brutal ways and provide them with the resources they need to use the euro freely, while liberating them from austerity. But most of their partners would view this outcome as a humiliating surrender. Far more likely then is a stand-off between an emboldened Greek government and its enraged creditors.

Such a stand-off would lead to a “stealth exit”. The banks would fail to reopen. Then the government would create some sort of (supposedly temporary) monetary instrument. Later still, people would see that the provisional arrangement had become permanent. Finally, albeit after much wrangling, Greece would have a new currency, but still be within the European Union.

Only one (or more) of three developments could block the path to an exit.

First, the Greeks could live with closed banks for the indefinite future. This is not impossible. But it is unlikely.

Second, the European Central Bank could expand its emergency lending to the Greek banking system. If the ECB were a normal central bank that is exactly what it would do. Greece has a run on its banks. As the lender of last resort, the central bank ought to lend into such a run. If the ECB believes the banks are solvent, it must lend. If the ECB believes the banks are insolvent, it should arrange recapitalisation — by converting non-insured liabilities into equity, by selling banks to new owners or by securing funding from the European Stability Mechanism (ESM).

Unfortunately, the ECB is not a normal central bank. It is the central bank of a half-baked currency union. By protecting itself against losses, the ECB risks recreating the redenomination risk that Mario Draghi’s “whatever it takes” speech of July 2012 was intended to eliminate. Fear creates what is feared.

Third, the eurozone governments could still reach a deal with Greece. This is what Athens is trying to achieve. But would it make sense for the eurozone? To answer this question one needs to consider how people now view the currency union itself.

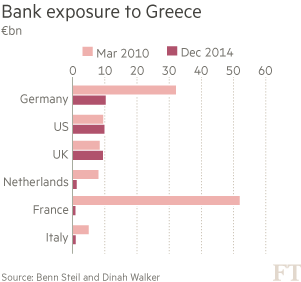

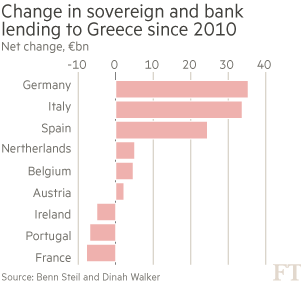

One way of thinking about the eurozone is as a zone of mutual solidarity. It is what the Greeks themselves appeal to. The reply of their creditors is that solidarity is built upon mutual obligations. The Greeks, they insist, cheated on their obligations, both before and after the crisis, so they do not deserve solidarity. This view is simplistic. Blame for the mess lies quite as much with irresponsible (mainly French and German) private lenders and with the governments that decided to provide the loans to Greece with which to bail those lenders out (see charts). This refinancing was of negligible benefit to Greece. The solidarity case for meeting halfway is powerful, particularly in view of the slump the Greeks have experienced.

An alternative view is transactional. Each country does what it believes to be in its own people’s interests. The reason for meeting Greece halfway would then be that the alternative — Grexit — would not merely guarantee a large default, but generate permanent instability within the eurozone. Shocks would lead to destabilising speculation. A currency union with an exit option is just a more rigid version of the old exchange-rate mechanism (ERM), vulnerable to debt crises in place of currency crises.

Some in core countries even seem to believe fear of such crises would impose valuable discipline upon irresponsible borrowers. Leaders of countries exiting from crises want to crush domestic political rivals who promise a soft exit from austerity. Meanwhile, France is on the other side. For the French, the currency union was the alternative to the ERM. If the eurozone allows for exit, its creation might have been for naught.

A big question, in sum, is whether the members of the currency union should want exit risk to be a core part of the eurozone’s construction. I think they should not because such a eurozone would be frighteningly fragile. In light of this risk, it is in the interests of members to seek a solution to the crisis that does not force exit at least until all alternatives are exhausted. They should also recognise that Greek debt is unsustainable. Debt relief is inescapable.

So what should the eurozone offer? Citi’s Willem Buiter has provided a possible plan. First, no more programmes. Second, the eurozone should use the ESM to pay off the maturing loans due to the ECB and International Monetary Fund, so dealing with the liquidity problems facing Greece over the next few years (see chart). Third, extend the maturities of outstanding official loans into the distant future and cap interest rates upon them. Finally, recapitalise Greek banks, if needed.

The Greek state would then depend on its ability to borrow in the market. If it could not borrow, it would have to balance its budget or create a new currency, so putting itself on the path to exit.

Greece is in the “last chance saloon”. The logic of where it is now is definitely towards the exit. But I remain unconvinced that this would be in the interests of Greece or of most other members of the eurozone. They should try an alternative. That would recognise the reality that further assistance with Greece’s debts is both right and sensible. It would find a way of protecting the banks from its state. It would then leave Greece to its own devices. The time devoted to this country should then be spent elsewhere. With debts manageable and the banking system sound, Greece may choose its own path, inside the eurozone or outside it. One last chance: that is it.

Martin Wolf

Fonte: FT

segunda-feira, 6 de julho de 2015

ECB should not make a deal harder to reach

FT tem razão: a decisão a respeito da saida da Grecia da UE não é técnica, mas política. Na minha modesta opinião é o momento da Merkel decidir como espera ser lembrada na historia europeia.

Even before Sunday’s referendum, Greece’s negotiations were in an advanced state of chaos. Its people overwhelmingly rejected an offer that had in any case expired. Prime minister Alexis Tsipras had urged a No vote, despite conceding most of the ground needed for the expiring deal. The crowds jamming Syntagma Square celebrated No as allowing austerity-free membership of the single currency. The more sullen interpretation from Greece’s creditors was it signalled a repudiation of Europe itself.

Had the Greek people voted differently, matters might now be clearer. Yet another result would only have brought a different variety of chaos. It may have forced Mr Tsipras off the stage, only to return within weeks at a new election, leaving exasperated creditors to strike a confused deal with the same band of recalcitrants.

As Greeks were thronging to their historic yet otiose plebiscite, the passage of time was threatening to settle matters. With deposits fleeing its banks, and funding from the European Central Bank capped, Greece’s government has been forced to impose capital controls, including a limit of just €60 per day on withdrawals.

Now this mess of clashing mandates and paradoxical demands threatens to ensnare the ECB. Its “emergency liquidity assistance” (ELA) is the fraying thread that still, just, binds Greece into the eurozone. For banks to reopen as promised, the ECB will need to lift its cap on ELA. But central banks are meant to lend only against high quality collateral, and without a new bailout the banking assets that underpin over €50bn of ELA are more like junk than sovereign debt.

But as ever in matters European there is room for interpretation. The ECB has a specific mandate to promote the smooth operation of payments systems, and a duty to promote the general economic policies of the EU. Both argue for it to keep shovelling funds towards Greek banks. In particular, untangling banks from their national sovereigns has been an EU policy goal ever since a fatal nexus of indebted states and shattered finance threatened the very existence of the single currency. Mario Draghi, ECB president, only ended that crisis in 2012 with his “whatever it takes” promise to stand behind sovereign debt.

Mr Draghi therefore has it within his power either to keep Greece on life support, or pull the plug. But it must not be his decision. Despite being embroiled in past bailouts — and hence a member of the loathed “troika” supposedly squeezing the Greek people — the credibility of the ECB remains essential to the eurozone. Governing a currency without the fiscal institutions to match, it has to rely on tools and instructions that are a work in progress. Were they complete, there would be jointly backed “eurobonds” to underpin Greek bank loans, and the ECB would not be in such an invidious position.

Mr Tsipras and Angela Merkel, the German chancellor, have agreed that Greece should put forward new proposals which, if agreed, might result in a third bailout package. The chances of success are slim, the odds having been lengthened by the referendum result which will have caused both sides to dig in their heels. Eurozone ministers, having lectured Greek voters about the risks of voting No, will want to avoid bowing to Syriza’s demands. But Mr Tsipras, under pressure from his hardliners and having charmed the Greek people with visions of an enhanced negotiating mandate, has staked too much to backtrack.

While there is even the slimmest chance of success, it should neither be the act nor the indecision of the ECB that finally drives Greece from the eurozone. Every day that passes, plummeting confidence and shuttered banks are propelling it into a downward spiral. If the Bank of Greece asks that the cap on ELA be lifted, Mr Draghi should urge the ECB governing council to agree and give the political negotiations the space to conclude. The financial risks are the same either way — eurozone governments already stand behind the ECB.

From first being allowed into the eurozone, through two bailouts to the cliff-edge posturing of Syriza this year, the decisions that have marked Greece’s sorry experience of the euro have been thoroughly political. If the saga now ends in Grexit it will be a political failure too. Mr Draghi’s role is to make that clear, and pass the buck to the politicians.

Editorial do FT

Even before Sunday’s referendum, Greece’s negotiations were in an advanced state of chaos. Its people overwhelmingly rejected an offer that had in any case expired. Prime minister Alexis Tsipras had urged a No vote, despite conceding most of the ground needed for the expiring deal. The crowds jamming Syntagma Square celebrated No as allowing austerity-free membership of the single currency. The more sullen interpretation from Greece’s creditors was it signalled a repudiation of Europe itself.

Had the Greek people voted differently, matters might now be clearer. Yet another result would only have brought a different variety of chaos. It may have forced Mr Tsipras off the stage, only to return within weeks at a new election, leaving exasperated creditors to strike a confused deal with the same band of recalcitrants.

As Greeks were thronging to their historic yet otiose plebiscite, the passage of time was threatening to settle matters. With deposits fleeing its banks, and funding from the European Central Bank capped, Greece’s government has been forced to impose capital controls, including a limit of just €60 per day on withdrawals.

Now this mess of clashing mandates and paradoxical demands threatens to ensnare the ECB. Its “emergency liquidity assistance” (ELA) is the fraying thread that still, just, binds Greece into the eurozone. For banks to reopen as promised, the ECB will need to lift its cap on ELA. But central banks are meant to lend only against high quality collateral, and without a new bailout the banking assets that underpin over €50bn of ELA are more like junk than sovereign debt.

But as ever in matters European there is room for interpretation. The ECB has a specific mandate to promote the smooth operation of payments systems, and a duty to promote the general economic policies of the EU. Both argue for it to keep shovelling funds towards Greek banks. In particular, untangling banks from their national sovereigns has been an EU policy goal ever since a fatal nexus of indebted states and shattered finance threatened the very existence of the single currency. Mario Draghi, ECB president, only ended that crisis in 2012 with his “whatever it takes” promise to stand behind sovereign debt.

Mr Draghi therefore has it within his power either to keep Greece on life support, or pull the plug. But it must not be his decision. Despite being embroiled in past bailouts — and hence a member of the loathed “troika” supposedly squeezing the Greek people — the credibility of the ECB remains essential to the eurozone. Governing a currency without the fiscal institutions to match, it has to rely on tools and instructions that are a work in progress. Were they complete, there would be jointly backed “eurobonds” to underpin Greek bank loans, and the ECB would not be in such an invidious position.

Mr Tsipras and Angela Merkel, the German chancellor, have agreed that Greece should put forward new proposals which, if agreed, might result in a third bailout package. The chances of success are slim, the odds having been lengthened by the referendum result which will have caused both sides to dig in their heels. Eurozone ministers, having lectured Greek voters about the risks of voting No, will want to avoid bowing to Syriza’s demands. But Mr Tsipras, under pressure from his hardliners and having charmed the Greek people with visions of an enhanced negotiating mandate, has staked too much to backtrack.