So what should the eurozone do now? Last week I concluded that the Greeks should vote Yes. They decided instead overwhelmingly to reject the terms of a deal that had been withdrawn. What might that mean? And how should the eurozone respond?

Apparently many, perhaps most, of those who voted believe their rejection would force a change of heart in the rest of the eurozone. Their partners would come to recognise the error of their brutal ways and provide them with the resources they need to use the euro freely, while liberating them from austerity. But most of their partners would view this outcome as a humiliating surrender. Far more likely then is a stand-off between an emboldened Greek government and its enraged creditors.

Such a stand-off would lead to a “stealth exit”. The banks would fail to reopen. Then the government would create some sort of (supposedly temporary) monetary instrument. Later still, people would see that the provisional arrangement had become permanent. Finally, albeit after much wrangling, Greece would have a new currency, but still be within the European Union.

Only one (or more) of three developments could block the path to an exit.

First, the Greeks could live with closed banks for the indefinite future. This is not impossible. But it is unlikely.

Second, the European Central Bank could expand its emergency lending to the Greek banking system. If the ECB were a normal central bank that is exactly what it would do. Greece has a run on its banks. As the lender of last resort, the central bank ought to lend into such a run. If the ECB believes the banks are solvent, it must lend. If the ECB believes the banks are insolvent, it should arrange recapitalisation — by converting non-insured liabilities into equity, by selling banks to new owners or by securing funding from the European Stability Mechanism (ESM).

Unfortunately, the ECB is not a normal central bank. It is the central bank of a half-baked currency union. By protecting itself against losses, the ECB risks recreating the redenomination risk that Mario Draghi’s “whatever it takes” speech of July 2012 was intended to eliminate. Fear creates what is feared.

Third, the eurozone governments could still reach a deal with Greece. This is what Athens is trying to achieve. But would it make sense for the eurozone? To answer this question one needs to consider how people now view the currency union itself.

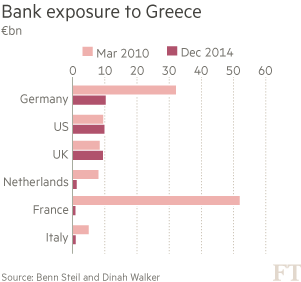

One way of thinking about the eurozone is as a zone of mutual solidarity. It is what the Greeks themselves appeal to. The reply of their creditors is that solidarity is built upon mutual obligations. The Greeks, they insist, cheated on their obligations, both before and after the crisis, so they do not deserve solidarity. This view is simplistic. Blame for the mess lies quite as much with irresponsible (mainly French and German) private lenders and with the governments that decided to provide the loans to Greece with which to bail those lenders out (see charts). This refinancing was of negligible benefit to Greece. The solidarity case for meeting halfway is powerful, particularly in view of the slump the Greeks have experienced.

An alternative view is transactional. Each country does what it believes to be in its own people’s interests. The reason for meeting Greece halfway would then be that the alternative — Grexit — would not merely guarantee a large default, but generate permanent instability within the eurozone. Shocks would lead to destabilising speculation. A currency union with an exit option is just a more rigid version of the old exchange-rate mechanism (ERM), vulnerable to debt crises in place of currency crises.

Some in core countries even seem to believe fear of such crises would impose valuable discipline upon irresponsible borrowers. Leaders of countries exiting from crises want to crush domestic political rivals who promise a soft exit from austerity. Meanwhile, France is on the other side. For the French, the currency union was the alternative to the ERM. If the eurozone allows for exit, its creation might have been for naught.

A big question, in sum, is whether the members of the currency union should want exit risk to be a core part of the eurozone’s construction. I think they should not because such a eurozone would be frighteningly fragile. In light of this risk, it is in the interests of members to seek a solution to the crisis that does not force exit at least until all alternatives are exhausted. They should also recognise that Greek debt is unsustainable. Debt relief is inescapable.

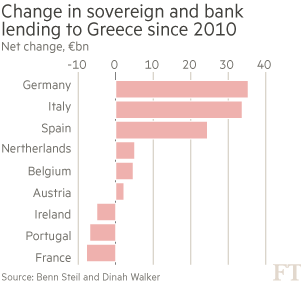

So what should the eurozone offer? Citi’s Willem Buiter has provided a possible plan. First, no more programmes. Second, the eurozone should use the ESM to pay off the maturing loans due to the ECB and International Monetary Fund, so dealing with the liquidity problems facing Greece over the next few years (see chart). Third, extend the maturities of outstanding official loans into the distant future and cap interest rates upon them. Finally, recapitalise Greek banks, if needed.

The Greek state would then depend on its ability to borrow in the market. If it could not borrow, it would have to balance its budget or create a new currency, so putting itself on the path to exit.

Greece is in the “last chance saloon”. The logic of where it is now is definitely towards the exit. But I remain unconvinced that this would be in the interests of Greece or of most other members of the eurozone. They should try an alternative. That would recognise the reality that further assistance with Greece’s debts is both right and sensible. It would find a way of protecting the banks from its state. It would then leave Greece to its own devices. The time devoted to this country should then be spent elsewhere. With debts manageable and the banking system sound, Greece may choose its own path, inside the eurozone or outside it. One last chance: that is it.

Martin Wolf

Fonte: FT