Why have oil prices fallen? Is this a temporary phenomenon or does it reflect a structural shift in global oil markets? If it is structural, it will have significant implications for the world economy, geopolitics and our ability to manage climate change.

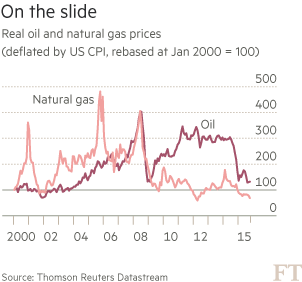

With US consumer prices as deflator, real prices fell by more than half between June 2014 and October 2015. In the latter month, real oil prices were 17 per cent lower than their average since 1970, though they were well above levels in the early 1970s and between 1986 and the early 2000s. (See charts.)

A speech by Spencer Dale, chief economist of BP (and former chief economist of the Bank of England) sheds light on what is driving oil prices. He argues that people tend to believe that oil is an exhaustible resource whose price is likely to rise over time, that demand and supply curves for oil are steep (technically, “inelastic”), that oil flows predominantly to western countries and that Opec is willing to stabilise the market. Much of this conventional wisdom about oil is, he argues, false.

A part of what is shaking these assumptions is the US shale revolution. From virtually nothing in 2010, US shale oil production has risen to around 4.5m barrels a day. Most shale oil is, suggests Mr Dale, profitable at between $50 and $60 a barrel.

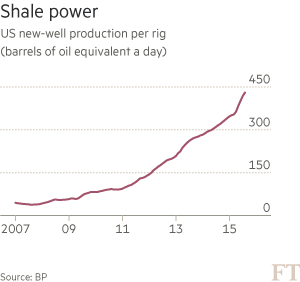

Moreover, the productivity of shale oil production (measured as initial production per rig) rose at over 30 per cent a year between 2007 and 2014. Above all, the rapid growth in shale oil production was the decisive factor in the collapse in the price of crude last year: US oil production on its own increased by almost twice the expansion in demand. It is simply the supply, stupid.

What might this imply?

One implication is that the short-term elasticity of supply of oil is higher than it used to be. A relatively high proportion of the costs of shale oil production is variable because the investment is quick and yields a quick return. As a result, supply is more responsive to price than it is for conventional oil, which has high fixed costs and relatively low variable costs.

This relatively high elasticity of supply means the market should stabilise prices more effectively than in the past. But shale oil production is also more dependent on the availability of credit than is conventional oil. This adds a direct financial channel to oil supply.

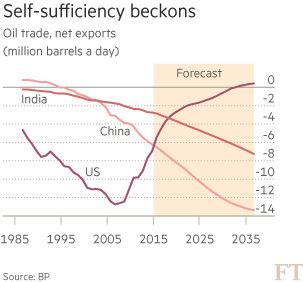

Another implication is a huge shift in the direction of trade. In particular, China and India are likely to become vastly more important net importers of oil, while US net imports shrink. Quite possibly, 60 per cent of the global increase in oil demand will come from the two Asian giants over the next 20 years.

By 2035, China is likely to import three-quarters of its oil and India almost 90 per cent. Of course, this assumes that the transport system will remain dependent on oil over this long period. If it does, it demands no great mental leap to assume that US interest in stabilising the Middle East will shrink as that of China and India rises. The geopolitical implications might be profound.

A further implication concerns the challenge for Opec in stabilising prices. In its World Energy Outlook 2015 , the International Energy Agency forecasts a price of $80 a barrel in 2020, as rising demand absorbs what it sees as a temporary excess supply. A lower oil price forecast is also considered, with prices staying close to $50 a barrel this decade.

Two assumptions underlie the latter forecast: resilient US supply and a decision by Opec producers, notably Saudi Arabia, to defend production shares (and the oil market itself). But the low-price strategy would create pain for the producers as public spending continues to exceed oil revenues for a long period. How long might this stand-off last?

A final set of implications is for climate policy. The emergence of shale oil underlines what was already fairly clear, namely, that the global supply capacity is not only enormous but expanding. Forget peak oil. As Mr Dale notes: “In very rough terms, over the past 35 years, the world has consumed around 1tn barrels of oil. Over the same period, proved oil reserves have increased by more than 1tn barrels.”

The problem is not that the world is running out of oil. It is that it has far more than it can burn while having any hope of limiting the increase in global mean temperatures over the pre-industrial levels to 2°C. Burning existing reserves of oil and gas would exceed the global carbon budget threefold. Thus, the economics of fossil fuels and of managing climate change are in direct opposition. One must give. Profound technological change might undermine the economics of fossil fuels. If not, politicians will have to do so.

This underlines the scale of the challenge leaders confront at the climate conference in Paris. But the response to the fall in oil prices shows how hopeless policymakers have been. According to the IEA, subsidies to the supply and use of fossil fuels still amounted to $493bn in 2014. True, they would have been $610bn without reforms made since 2009. So progress has been made.

But low oil prices now justify elimination of subsidies. In rich countries the opportunity of low prices could — and should — have been used to impose offsetting taxes on consumption, thereby maintaining the incentive to economise on use of fossil fuels, increasing fiscal revenue and allowing a reduction in other taxes, notably on employment. But this important opportunity has been almost entirely missed.

One has to ask whether there is the slightest chance that effective action, rather than window-dressing, will emerge from Paris. I hope to be proved wrong, But I am, alas, sceptical.

Martin Wolf

Fonte:FT